I will admit to being a skeptic when a new product starts making the rounds on Wall Street. After a long time in this business, I have learned that a lot of what comes out of that world is built around what will sell, not necessarily around what works. Filtering the noise from the substance is a large part of what we are paid to do as advisors.

Wall Street’s product cycle tends to move in themes, and one theme we have seen a lot of lately is a positive one: strategies designed to be more tax aware. Many are overly complex and too costly. But two have caught our attention recently because they appear to have real potential.

Neither will be right for every investor, and both carry their own risks and drawbacks. But both offer interesting answers to a problem many investors are facing right now. After years of strong markets, a lot of people are holding portfolios with large unrealized gains, often concentrated in just a few names. They would like to make changes, but the tax cost of selling keeps them stuck. These two strategies approach that same question from different angles: how do you reposition a portfolio without handing a large share of it to the IRS along the way?

351 Exchanges

The first strategy is the 351 exchange. Conceptually, it is similar to what real estate investors do with a 1031 exchange, swapping one investment or portfolio for another without triggering capital gains.

For some background, the mechanics behind the 351 exchange are the same ones that have long made ETFs more tax efficient than traditional mutual funds. The provision has been on the books for many years, and it is how ETFs manage fund flows without triggering gains or losses every time shares are created or redeemed.

The 351 exchange solutions being marketed today are tax deferral strategies. They allow an investor to make a one-time portfolio adjustment without an immediate tax consequence.

These tend to fit a taxable investor who holds a portfolio of highly appreciated securities, wants to change how they are invested, and feels stuck because of the tax cost. We see this often with portfolios that have become heavily concentrated in U.S. technology stocks, names like Microsoft, Amazon, or Nvidia. Those positions have performed well, which is a good problem to have, but it also means they can represent an outsized share of a portfolio. When that happens, the portfolio’s risk level often no longer matches the risk the investor actually wants to carry.

A 351 exchange can help address that. The investor exchanges some or all of their appreciated holdings for shares in a newly issued 351 exchange ETF, one that better fits their needs, their current view, or simply offers better diversification. After the exchange, they own ETF shares carrying their original tax lots and unrealized gains, but their performance going forward reflects the return of the ETF, not of the holdings they contributed.

It will not fit every situation, and not every portfolio will even qualify. To participate, an investor must contribute a portfolio that meets several criteria:

- Eligible holdings. Only cash, individual stocks, and ETFs can be contributed. Mutual funds and partnerships do not qualify.

- Single-position limit. No single stock can represent more than 25% of the portfolio being contributed.

- Top-five limit. The five largest single-stock positions together cannot account for more than 50% of what is contributed.

There are also several considerations to weigh before pursuing one:

- Regulatory scrutiny. These exchanges have started to draw more attention from the IRS and the U.S. Treasury Department. The rules could change, and investors should understand that risk going in.

- Intent of the fund. One of the trickier aspects of the rules is that the new ETF is not supposed to have a plan to dispose of the contributed assets. Yet many funds being launched appear to target mandates that all but guarantee the portfolio will need to be adjusted. It is reasonable to expect this area will receive closer review over time.

- Long-term commitment. The investor really must want to be a long-term owner of the new ETF. The initial transition may not trigger a gain, but future liquidity will require selling ETF shares, and that will generate gains.

Given the legal and tax uncertainty, we have not yet used any of these vehicles. But it is a strategy we are watching closely. Under the right circumstances, it has the potential to be a very good solution.

Equity Long/Short Extension Strategies

The second strategy does not have a common industry name the way the 351 exchange does. We refer to it as an equity long/short extension strategy. To understand it, it helps to start with the strategy that laid its foundation.

One of the bigger terms in wealth management over the past five-plus years has been “direct indexing.” Most investors are already familiar with index investing, where you buy a single fund that tracks an index like the S&P 500 and, for a small fee, earn close to that index’s return with instant diversification.

Direct indexing is an evolution of that idea. Instead of owning one fund, the investor owns all or a representative sample of the underlying stocks in the index directly. It adds cost and complexity, but it also creates real advantages, including some customization and, most importantly, more opportunities for tax-loss harvesting.

With a traditional index fund, you can only harvest losses when the whole index is down. In reality, even strong years produce winners and losers. In 2025, for example, the S&P 500 rose nearly 18%, yet 171 stocks in the index declined. Owning the names directly lets an investor sell those losers and bank the losses, which can create future tax savings.

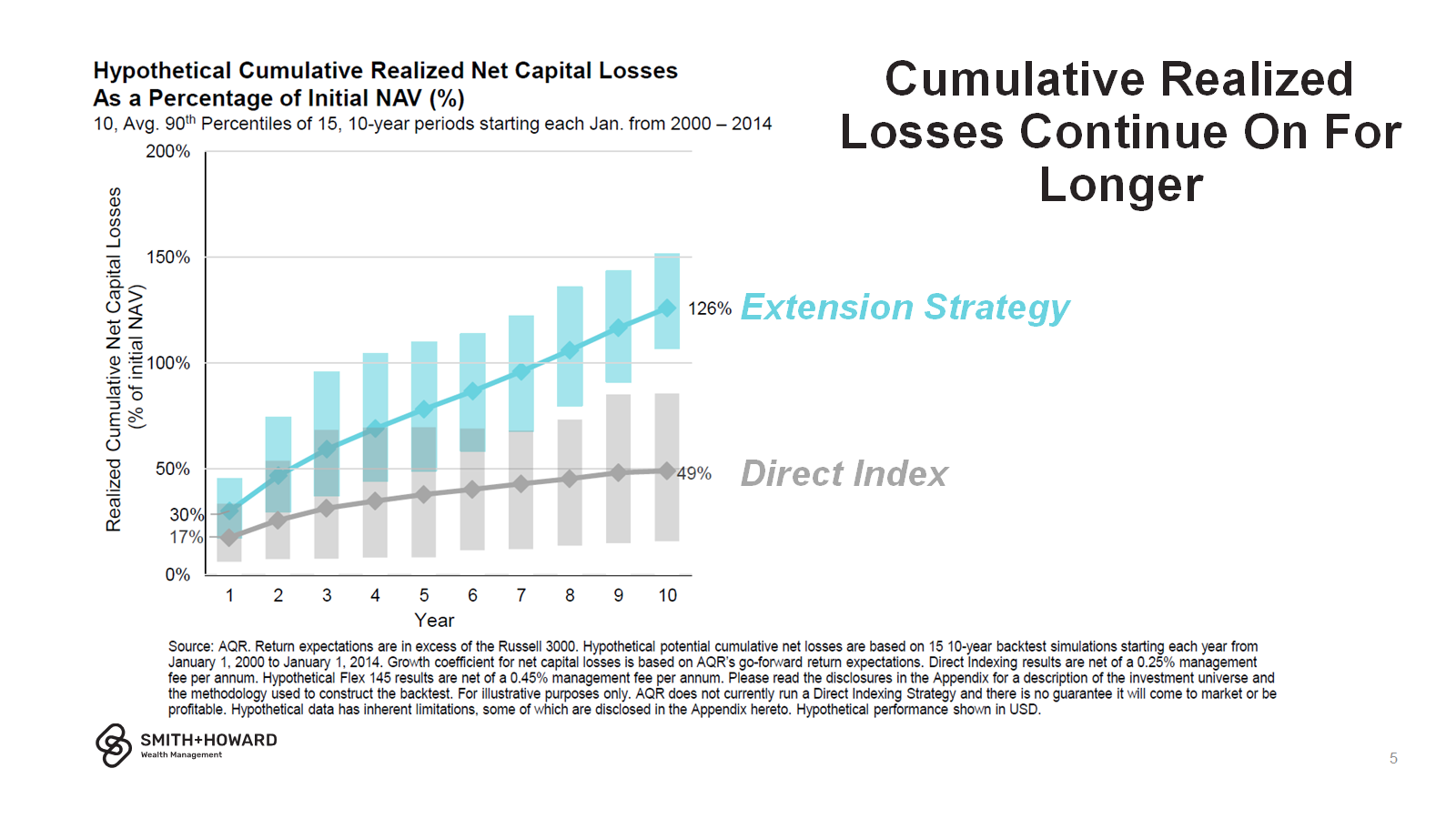

Direct indexing has a drawback, though. Because markets tend to rise over time, the portfolio can eventually become “ossified.” As prices climb, the opportunities to harvest losses fade, and the investor is left holding a portfolio that costs more than an index fund and no longer closely tracks the index, unless they are willing to realize gains to adjust it. With U.S. equities performing so well over the past decade, ossification became a real problem, and that is where the long/short extension strategy enters the picture.

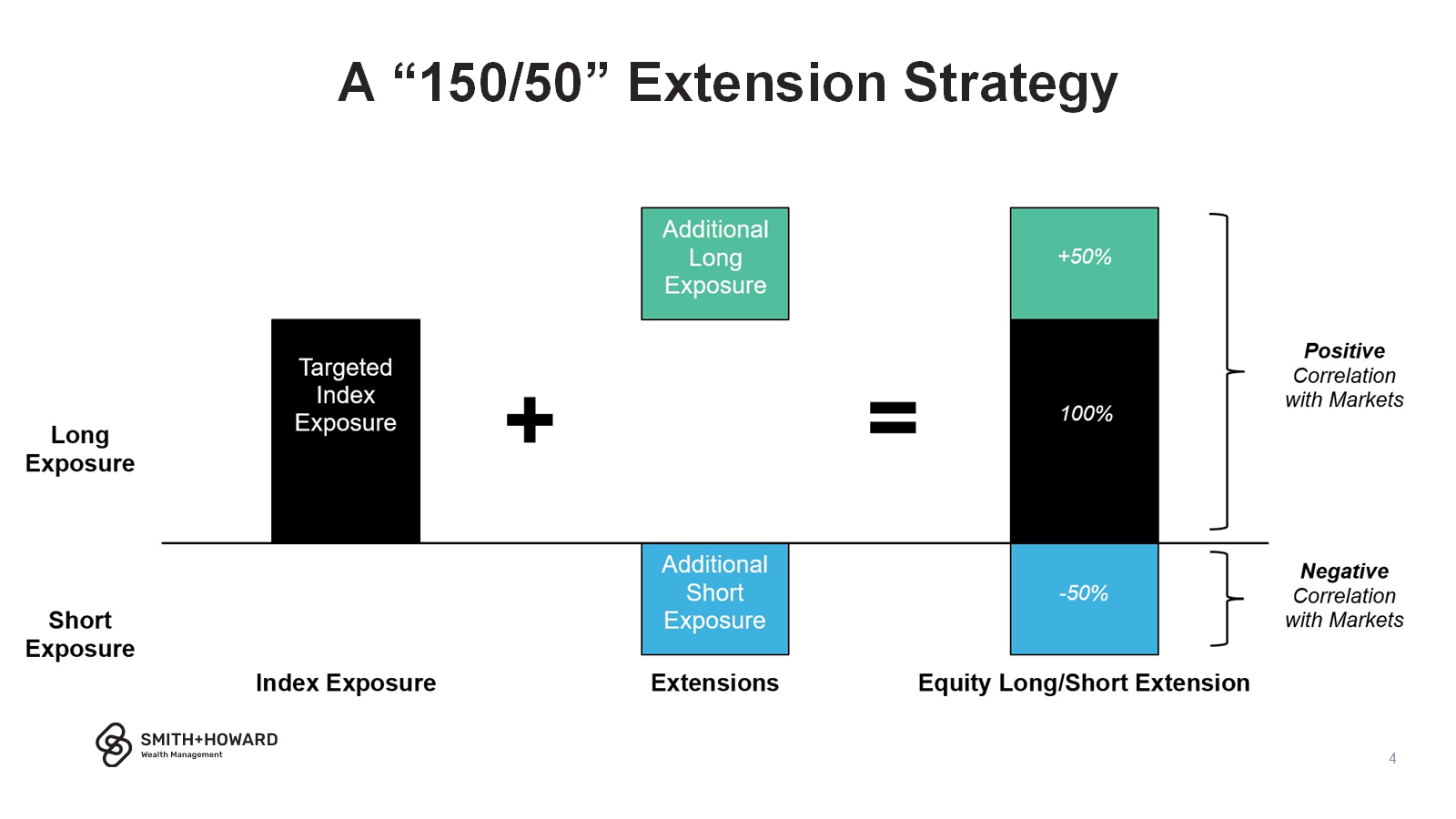

In short, this is direct indexing with more horsepower. Alongside an equity position that mimics an index like the S&P 500, the manager uses portfolio margin to also buy additional stocks expected to outperform and short stocks expected to underperform, with those additional long and short positions offsetting one another.

In what is called a 150/50 extension, for every $100 invested the manager buys $150 of stocks and shorts $50. The net market exposure stays at $100, even though the gross positions add up to $200.

The investor still expects to participate fully in market returns, possibly even to outperform. The real shift is in tax-loss harvesting, both in how much is available and in how long it lasts. The additional capital at work produces larger realized losses than standard direct indexing and makes the direction of the market less relevant. Whether the market rises or falls, opportunities to harvest losses are expected to remain. That also makes ossification far less of a concern. Estimates from one manager show how quickly the harvesting opportunity fades in a direct indexing approach, while in the extension strategy it continues at a meaningful level.

This strategy is more complex, it uses leverage, and it costs more. It is not for everyone, and account minimums are currently quite high. On the other hand, there is less legal and tax uncertainty here. Long/short strategies have existed for a long time. What is new is the focus on tax efficiency rather than purely on pretax returns.

The Most Important Point

We are sent investment ideas constantly, and most we can set aside quickly. These two caught our attention. At a minimum they are worth understanding, and for an investor holding a portfolio of highly appreciated securities that no longer fits their needs, they may be significant.

Which brings me to the most important point. Neither of these is a yes-or-no answer. Whether a 351 exchange or a long/short extension actually fits depends entirely on your situation: your gains, your concentration, your time horizon, your tolerance for complexity and risk, and how the tax math works out for you specifically.

That is the part we take seriously at Smith + Howard. These strategies sit exactly where investing and tax planning meet, and getting them right means having the right people at the table, investment and tax professionals working the same problem together, so that something that looks good on the surface actually holds up against your full financial picture. The goal is not to chase the newest product. It is to make sure that if you use one, it is the right one for you, and that you keep more of what you have worked to build.

If either of these could be a fit for you or someone you know, we would welcome the conversation.

Smith + Howard Wealth Management serves as your family CFO, guiding clients toward wise, well-informed decisions across every aspect of their financial lives, including investment management, tax planning, financial planning, estate planning, and portfolio administration. Driven by a core set of values, we strive to fulfill our mission: we provide financial peace of mind.

This article is for informational purposes only and does not constitute investment, tax, or legal advice. Specific securities are mentioned solely for illustration and are not recommendations. Any strategy described here should be evaluated against your individual circumstances in consultation with your advisor.

July 1, 2026

July 1, 2026

Back to Insights

Back to Insights