Writing about the U.S. equity market in anything less than glowing, optimistic terms is incredibly difficult and almost unnatural. So much so, that I have started and stopped this piece several times over the past few weeks.

Before you panic, this isn’t some doomsday article. In fact, the thoughts expressed in this article pertain to the very long term – think decades, not the next few months, quarters or even years. The U.S. economy and equity market has quite a lot going for it presently, especially relative to other economies and markets. Despite all the U.S. may have going for it, there are bound to be challenges and changing dynamics that impede returns. As you read along, you’ll see that we look at two such potential long-term obstacles. Interestingly, both have been tailwinds for stocks for multiple decades, but recently have started to look more and more like headwinds.

Those two items are interest rates and corporate tax rates. Companies have enjoyed the fact that both have been on a predominantly downward path since the mid-1980s. As both rates fell, it effectively allowed more of every dollar of revenue to drop to the bottom line. While neither has seen a big shift yet, it’s becoming increasingly clear that, at best, the two can no longer be expected to provide the same type of earnings boost in the future. Will either completely upend equity markets? Not likely. They could, however, be a drag on earnings growth and that would eventually impact equity returns.

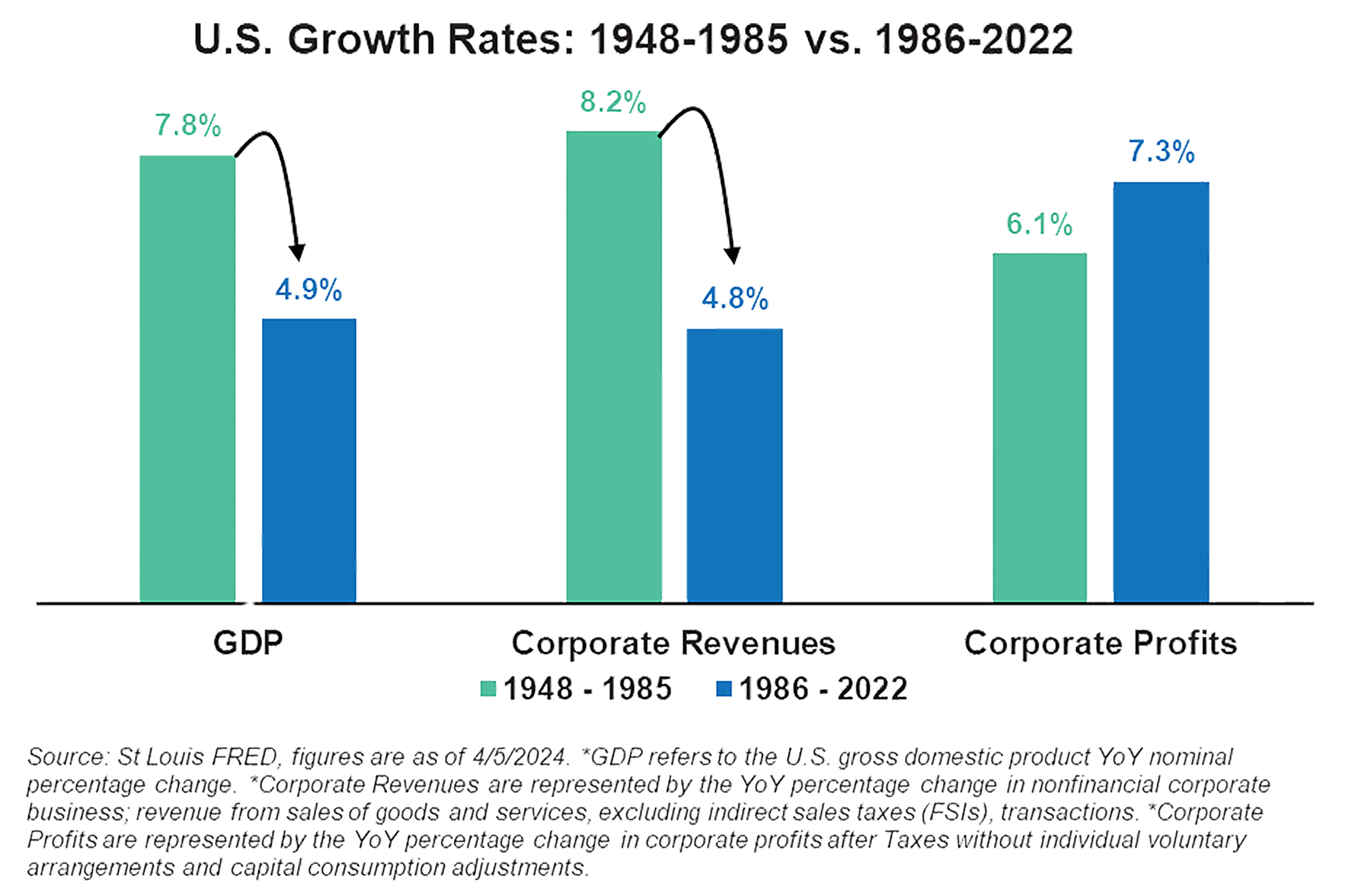

Falling interest and tax rates certainly weren’t the only tailwinds for corporate profitability over the last couple of decades, but we think they played a large role in the obvious disconnect shown in the following graph.

The economy is not the market, of course, but we would expect to see similar trends and levels of growth when comparing the broad economy with corporate America. We see that with the growth rates of GDP, corporate revenues, and corporate profits from the post-WWII era through the mid-80s (mint green bar, 1948-1985). In the period from 1986-2022 (blue bar), however, that same pattern does not hold. GDP growth and corporate revenue growth slowed materially and at similar rates or to similar levels, but corporate profit growth actually accelerated. Interest rates and tax rates weren’t the only reasons, but we think they explain a lot of that divergence. If that is true, then it logically follows that a change in which those two variables move higher would have the opposite impact on future profit growth. Instead of providing a boost, they become a drag.

Corporate Tax Rates

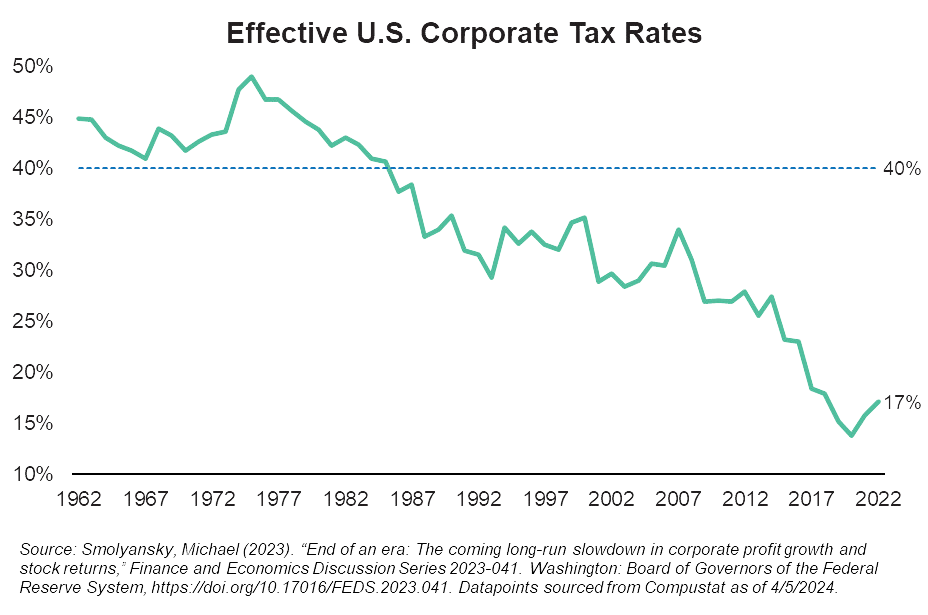

Let’s look first at the less complicated of the two, corporate tax rates.

The impact of lower corporate tax rates on the bottom line is relatively straightforward. The smaller the government’s cut of pre-tax profits, the larger the amount remaining as after-tax profits for shareholders. After bouncing between the low and high 40% level from the 1960s through the early 1980s, the effective corporate tax rate broke below 40% in 1986 and has slowly, but meaningfully, drifted lower for the past 40 years. It ultimately fell to a low of just 14% in 2020, more than 70% below its highest level back in 1975.

The last big shift in corporate taxes occurred with the 2017 Tax Cuts and Jobs Act which dropped the stated corporate tax rate from 35% to the current 21%. Absent an extension of that provision in the Act, however, the rate will automatically “sunset” or revert to prior levels in 2026. Corporations have about a year and a half to enjoy the lower rates, but change appears imminent. Even if we don’t see a complete reversal in tax rates, the boost to earnings that companies have enjoyed from a falling tax rate for more than 40 years may finally be maxed out.

Corporate Leverage and Interest Rates

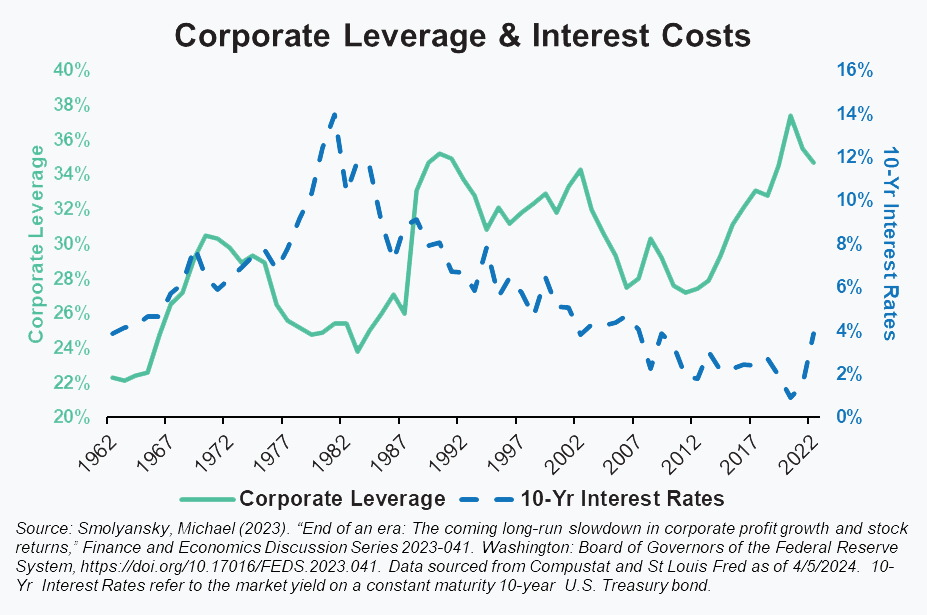

The impact of interest rates and their associated debt costs is a little more nuanced and is also where we are already seeing a shift.

Similar to what we noted with corporate tax rates, interest rates (the dotted blue line) have been falling since the early 1980s. All else being equal, falling rates mean falling interest costs and rising bottom-lines.

The complicating factor or nuanced aspect here is that as the cost of debt fell, companies also increasingly funded themselves via debt, seen in our graphic as the corporate leverage percentage (mint green line). Not only was every dollar of debt less and less costly over the years, but companies were able to squeeze the proverbial lemon even more by taking advantage of that low-cost debt to a greater degree.

Unlike with corporate tax rates, interest rates are already shifting and we do expect to see debt costs increase. That is evident on the far-right hand side of the graph and the recent spike in the dotted blue line tracking the yield of the 10-year U.S. Treasury bond. Interest rates all along the yield curve, including the 10-year, have already moved meaningfully higher. This move higher in interest rates and bond yields won’t completely or immediately reverse the cost benefits companies have enjoyed, though. Recognizing that interest rates were at historically low levels most companies took advantage of the prior environment and issued debt that won’t need to be paid off for years. Many companies were able to lock in those low financing costs and will only need to deal with today’s higher rates when they need to refinance or issue new debt.

The change in interest costs is coming, but it’ll be more of a gradual transition than a sudden shock.

Estimating the Impact

My 16-year-old daughter likes to say at some point during any of our conversations “so what’s your point?”. As I mentioned at the outset, this isn’t a doomsday situation or something we expect to completely derail equity markets. Our long-term return expectations for stocks are still positive. We do, however, think that U.S. equity investors may need to lower expectations.

How much lower is obviously the question. Given our multiple decade timeframe and all the moving parts, it would be foolish to aim for precision, but we can still look at it from an “orders of magnitude” mindset.

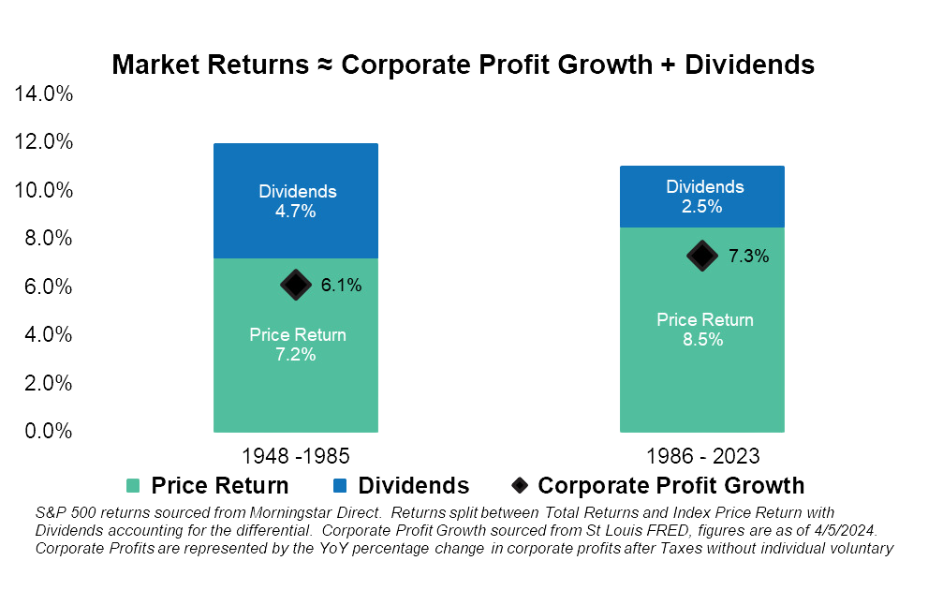

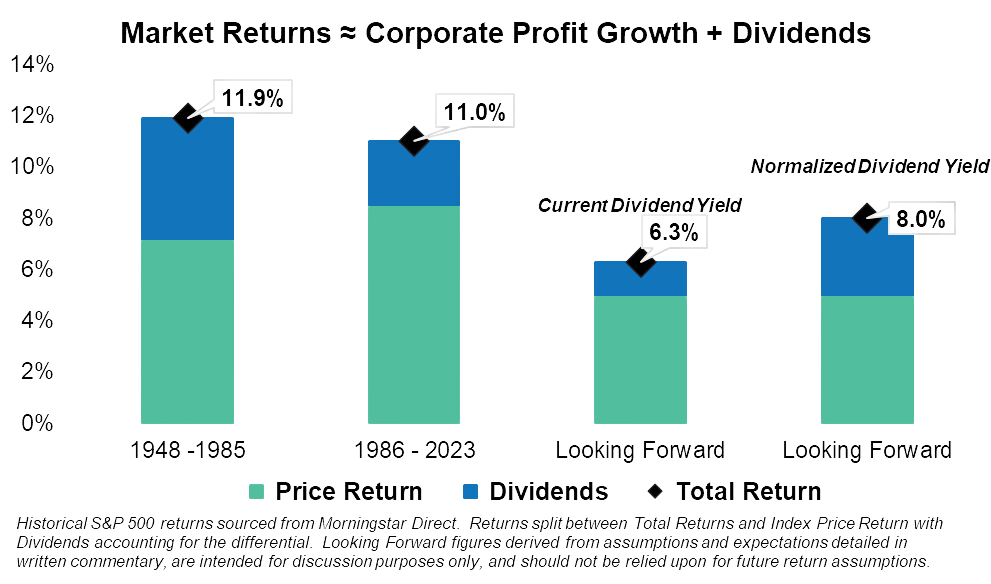

Over very long periods of time (again, decades, not years) it’s reasonable to expect equity returns to loosely track corporate profit growth + dividends. If we go back to the numbers from our first graph comparing the periods of 1948-1985 and 1986-2022, we can see how that played out over those two periods. It will never line up exactly, of course, since we’re comparing corporate profit growth for the broader economy (which includes companies of all sizes) with the returns of the S&P 500 (only large cap companies), but for this discussion, it is certainly “close enough.”

Despite some expected variance, corporate profit growth (black diamond) aligns fairly closely with the price return portion of the S&P return (mint green portion of the bar) for both time periods.

As we saw in the section on GDP and corporate growth rates, corporate profit growth since 1985 diverged from the broader economy and corporate revenue growth rates. If, as we suspect, falling interest and tax rates drove a lot of that divergence, then if the boost from those two items were to go away (or even reverse) we could reasonably expect corporate profit growth to fall back in closer alignment with economic and corporate revenue growth rates in the future.

A forward-looking estimate for equity returns would then hinge on 1) an estimate of price return derived from the growth rate of the overall economy and corporate revenues and 2) the expected dividend yield.

Estimating the growth rate for the economy and corporate revenues is, of course, no easy task, but for purposes of this exercise we think it’s fair to round up slightly from the nominal growth rate we’ve experienced since 1986 (4.8-4.9%) and use a 5.0% figure. The U.S. economy has certainly had its ups and downs since 1986, but smoothing the data by using multiple year moving averages shows the 5% figure to be a reasonable assumption and consistent with current data. After all, order of magnitude is more our goal than is precision.

For the dividend yield, we’ll demonstrate using two different approaches. The simplest version would be to use the current dividend yield of the S&P 500 Index, which is approximately 1.3%. A straightforward and presently applicable approach, it may yet be too conservative in the long run as it doesn’t account for the fact that dividend payout decisions are also tied to corporate profit growth, as well as interest and tax rates. If we expect some normalization of interest and tax rates and a corresponding slowing of corporate profit growth, we should recognize that we may also see a normalization in dividend yields (higher). Slower corporate profit growth typically means companies will return more cash to shareholders rather than reinvesting it back into the business. It’s probably no coincidence that dividend yields for stocks have also trended lower since 1985. In many ways their path mirrored that of interest and tax rates. Prior to 1985, dividend yields were rarely ever below 3% so we don’t think it would be unreasonable to see them return to those levels. As a result, our Looking Forward figures in the following graph are broken out into two separate dividend assumptions: one using the current 1.3% yield and the other the “normalized” yield of 3%.

If the numbers in this graph make you question my assertion that this isn’t a doomsday article, don’t be alarmed and do keep reading. An estimate of future equity returns that is nearly 30-40% below what investors have enjoyed historically might be considered pretty dire, if not downright depressing. We do think investors should adjust their expectations for returns lower, however, the figures in this graph likely overestimate what that adjustment truly needs to be for several reasons:

This assumes that the entire boost to corporate profit growth was driven by lower interest and tax rates. Even though we believe they played a significant role in keeping profit growth elevated while the general economy and revenues slowed, there were also other drivers that aren’t necessarily going away – lower labor costs, productivity growth, stock buybacks, etc. There may also be new drivers like AI, that can act as new catalysts.

The boost to the bottom line from lower taxes and interest rates may have “maxed out”, but they also aren’t going to simply reverse immediately or completely. As we mentioned, the impact of somewhat higher interest rates will be felt gradually over the course of many years.

As we detailed with our separate dividend assumptions, there are likely other things that were negatively impacted by falling tax and interest rates. Things that might have direct or indirect positive implications for the economy or corporate revenues and profits. A positive offset, if you will, to the headwinds of normalizing tax and interest rates.

Although we aren’t anticipating that earnings multiples will expand (rise) from current levels, this exercise does ignore their impact on investor returns.

Regardless of whether the impact ends up being 2% or 5%, the prevailing theme is that these two variables have likely flipped from tailwind to headwind for U.S. equity markets. While their impact is likely to be felt gradually and over a very lengthy period, that doesn’t mean they should be dismissed. It is easy for investors to focus more on what is happening in any given quarter or year, but to use a popular expression, we believe that can lead one to “miss the forest for the trees.”

That may be especially important today for U.S. investors. As U.S. based investors, we all tend to have a natural home-country bias and recent returns have only led to a greater level of confidence in the “home” market. Even with the selloff in 2022, the U.S. equity market has returned an annualized 14% since 2009 and the end of the great financial crisis. That’s several percent higher than the historical norm and places it among the best performing markets globally. As a result, many investors, and even some financial advisors, have given up on international equities and diversification more generally. Both of which we find troubling and expect will prove a costly mistake in time.

It wasn’t that long ago, but investors seem to have forgotten how poorly U.S. equities did from 2000 thru 2009. It’s sometimes referred to in the investment industry as the lost decade for U.S. equities, as the S&P 500 lost roughly 1% a year over a 10-year period. Plenty of other asset classes and areas of the market made money during that same period – so positive returns or U.S. market outperformance is certainly not a given. Too many investors (in our opinion) seem to have forgotten that period and the lessons learned from it in regard to diversification.

We aren’t necessarily arguing that the U.S. is set for some period of prolonged underperformance. Rather we want to make sure investors maintain perspective and don’t become complacent or overconfident when it comes to any one asset class or market. Today, that market for most investors seems to be U.S. large cap equities. That can be easy to do when returns have been as strong as they have for as long as they have, but as we’ve shown throughout this piece there is a growing set of headwinds that may make repeating that performance difficult going forward.

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Want to get insights right to your inbox?

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

August 26, 2024

August 26, 2024

Back to Insights

Back to Insights