Over the past several months, we continuously emphasized the importance of not letting politics shift ones’ investment approach or focus on the long-term. Much like trying to time the market, investing based on a view of who will win an election or how the market will react to an election is one of the biggest mistakes we see investors repeatedly make. Staying the course can be easier said than done, though, as elections can trigger strong emotions, and nothing derails a well-crafted investment plan and portfolio faster than emotions.

Even after the election, for many, emotions intensify rather than subside. For those for whom that is the case, our message is not geared towards telling anyone what or how to feel. We are all entitled to process things in our own way and on our own timeline.

Rather, our message seeks to help all investors think about and navigate a post-election environment. We’ll dive into some specifics on policy and the potential impact to stocks and bonds, but big picture, our message and investment approach doesn’t change post-election. Our focus, as it always has been, will be to stick to an approach rooted in valuations and the long-term.

Policy Initiatives

The morning after the election, my inbox was predictably full of outlook commentary and invitations to conference calls from a who’s who of Wall Street investment banks and asset management firms. Over the years, I’ve culled down the list of firms and people that I find the most insightful and I did my best to read their commentary or listen to their calls.

There was one consistent theme that I thought was an excellent reminder: Candidates make a lot of promises on the campaign trail, but no administration gets everything they want. Compromises are made and campaign promises eventually get prioritized, often by what can be effected the quickest. In the case of a second Trump administration, that likely means an early focus on immigration and tariffs, given that the President has considerable leeway to act via Executive Orders.

Immigration

With regard to immigration, President-elect Trump’s hard-line approach was a central theme to his campaign. He expressed a desire to enact a mass deportation program, resume building the border wall along the southern border, and ending automatic citizenship for children of undocumented immigrants born in the U.S.

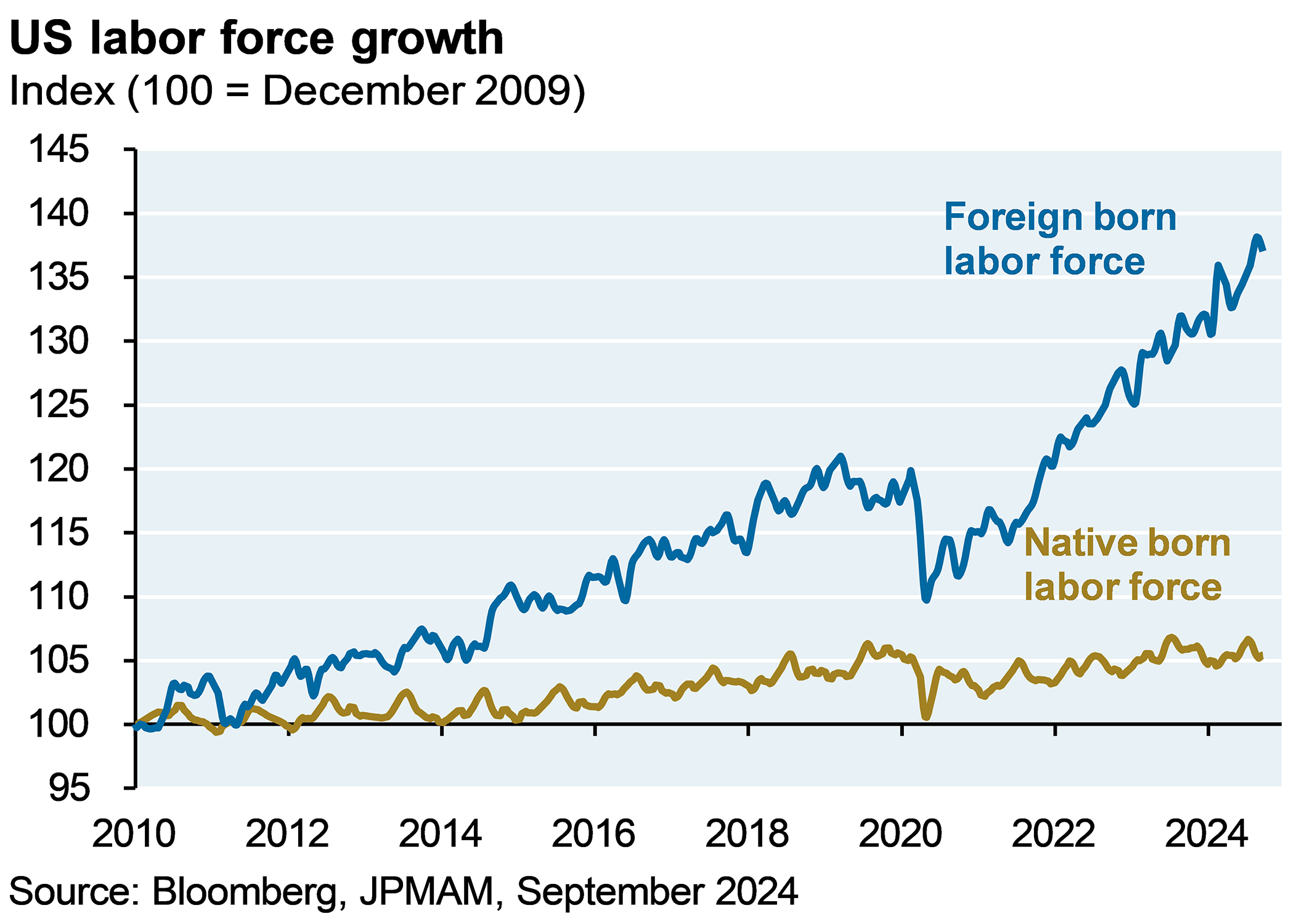

The long-term implications of each are unknowable, but the mass deportation program is probably the most notable from a short-term economic perspective. Sectors like hospitality, construction, agriculture, and others are heavily reliant upon immigrants for their labor force. More broadly, the economy and its growth has become increasingly reliant on immigrants over the years as this graph shows.

Note: The Foreign born labor force in the above graph does not make a distinction between legal and illegal immigrants.

The economy may be complicated, but economic growth at its core is a pretty straightforward calculation with the two main inputs being worker productivity and the growth in the number of workers. With worker productivity and U.S. birth rates both dropping over the last few decades, our economic growth has been increasingly dependent upon the rise in foreign born labor.

That dynamic is unlikely to derail such policy initiatives, but it could alter how quickly and aggressively they are implemented. Pre-election polling showed that there was a greater level of confidence in candidate Trump when it came to the economy, so the administration will undoubtedly consider the economic implications of its immigration policies.

Tariffs

Tariffs were also a central theme of Trump’s campaign. He has proposed a universal baseline tariff of 10%, a tariff increase of “more than 60%” on Chinese goods, a 100% tariff on cars made outside the U.S., and tariffs aimed at penalizing companies that outsource U.S. jobs.

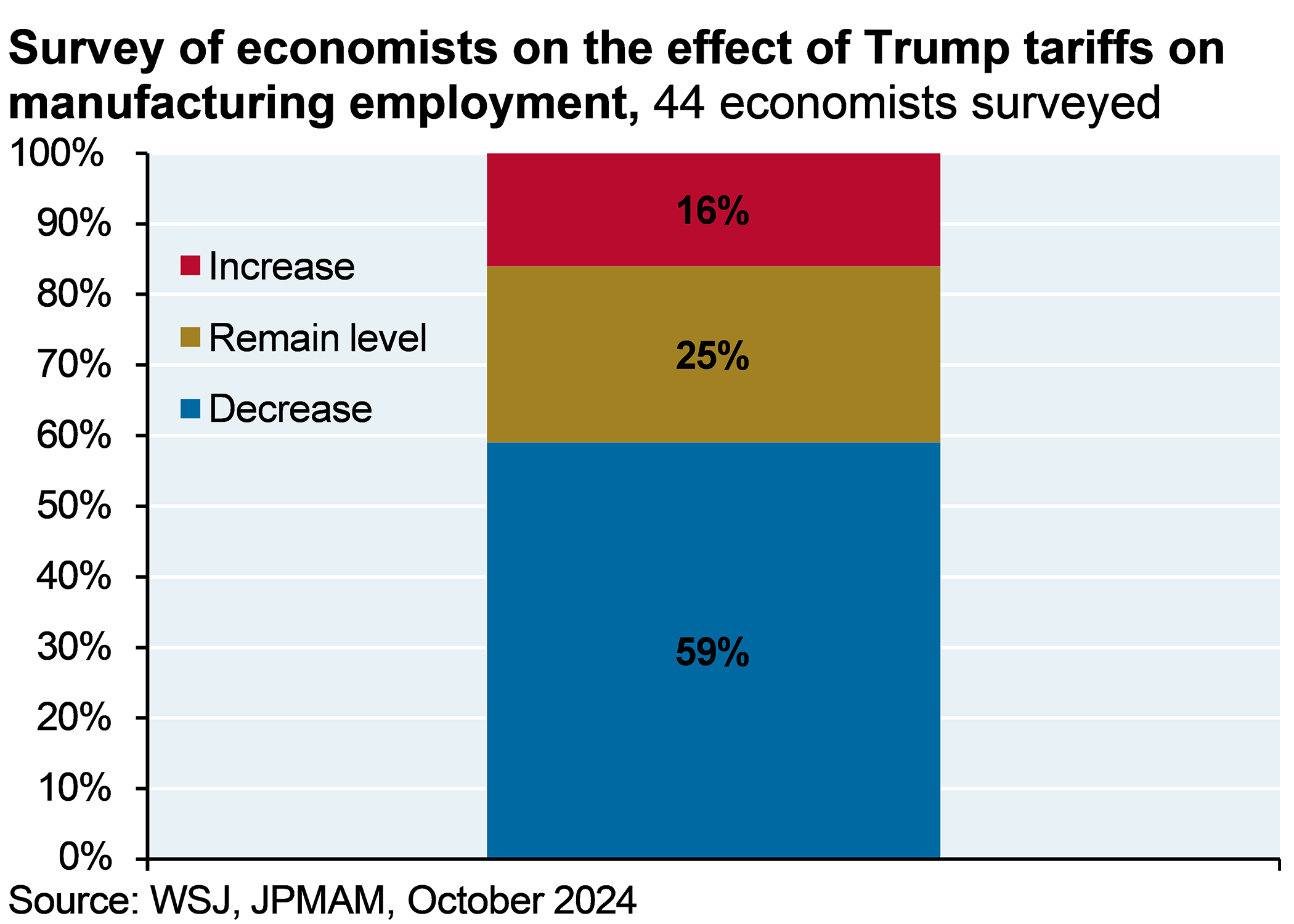

While an increase in tariffs appears relatively certain, there are some legal constraints on what the President can do via Executive Order and many prognosticators have speculated that these proposals may just be a starting point or a negotiating tactic. What actually gets implemented is likely to be less severe and, similar to immigration, the administration will need to weigh the economic implications. As the following graph shows, only 16% of economists in a recent poll expected the tariffs to positively impact the number of manufacturing jobs in the U.S. Nearly 60% thought they’d actually have a negative impact.

Immigration and tariffs are two policy initiatives that President-elect Trump has more control over, but they are far from his only policy proposals. Here is a quick rundown of some of the other policy initiatives.

Tax, Monetary and Fiscal Policy

Tax policy

Cut funding for the Internal Revenue Service

Cut corporate tax rate to 15% for companies that produce goods in the U.S.

Remove tax on Social Security benefits, tip income, and overtime pay

Extend the parts of the Tax Cuts and Jobs Act (TCJA) that are set to expire

With Republicans in control of the White House and both chambers of Congress, there is likely to be broad support for such initiatives. With that said, the majorities are slim and there are still some Republican deficit hawks that may push for scaling some of the initiatives back. As such, it would not be surprising to see the early focus be on some of the areas where there may be bipartisan support, such as eliminating taxes on tips and extending tax cuts that would keep taxes from increasing for those making $400k or less.

Monetary Policy (Federal Reserve, the Fed)

Could resume pressure/rhetoric toward the Federal Open Market Committee pushing for a faster reduction in short-term interest rates

Push for plans to make the Fed less independent

Appoint a new Fed Chair when Jerome Powell’s term expires in 2026

With the Fed already having started to cut short-term interest rates and the economy seemingly on track for a soft landing, it’s possible that President-elect Trump will focus his attention elsewhere – at least for the time being.

Fiscal Policy

Rein in government spending on foreign aid, clean energy, and immigration

Protect Social Security and Medicare from benefit cuts

Establish “Department of Efficiency” under Elon Musk with goal of cutting $2 trillion in spending

Market Implications

Financial markets had a swift and meaningful response to the election even before they opened on Wednesday morning. Stocks surged higher on the prospects of pro-growth policies and deregulation. Interestingly, that reaction was the complete opposite to what happened in 2016 when then candidate Trump defeated Hillary Clinton. In 2016, equity market futures cratered in the middle of election night as a Trump victory became clear before ultimately recovering during the next trading day.

While equity markets embraced some of the positive possibilities of a 2nd Trump term, bond investors had a very different reaction. Worried about the implications of tariffs and rising deficits, the yield on the 10-Year U.S. Treasury climbed from 4.29% to as high as 4.75% mid-day before closing at 4.43%. That initial surge higher in yields may have proved short-lived, but the one-day move of 14 basis points for the 10-Year and the return of -0.74% for the U.S. bond benchmark index shows that the implications for markets may differ.

At the outset of this note, we reiterated our view that investors should stay the course and not make major portfolio changes in response to the election or potential policy changes. This feels like a good time to revisit that viewpoint. Telling investors to look past the new administration’s policy initiatives is not the same as saying policy doesn’t matter. Policy can absolutely have an impact – but it’s often not the impact many expect or the biggest determinant of future returns.

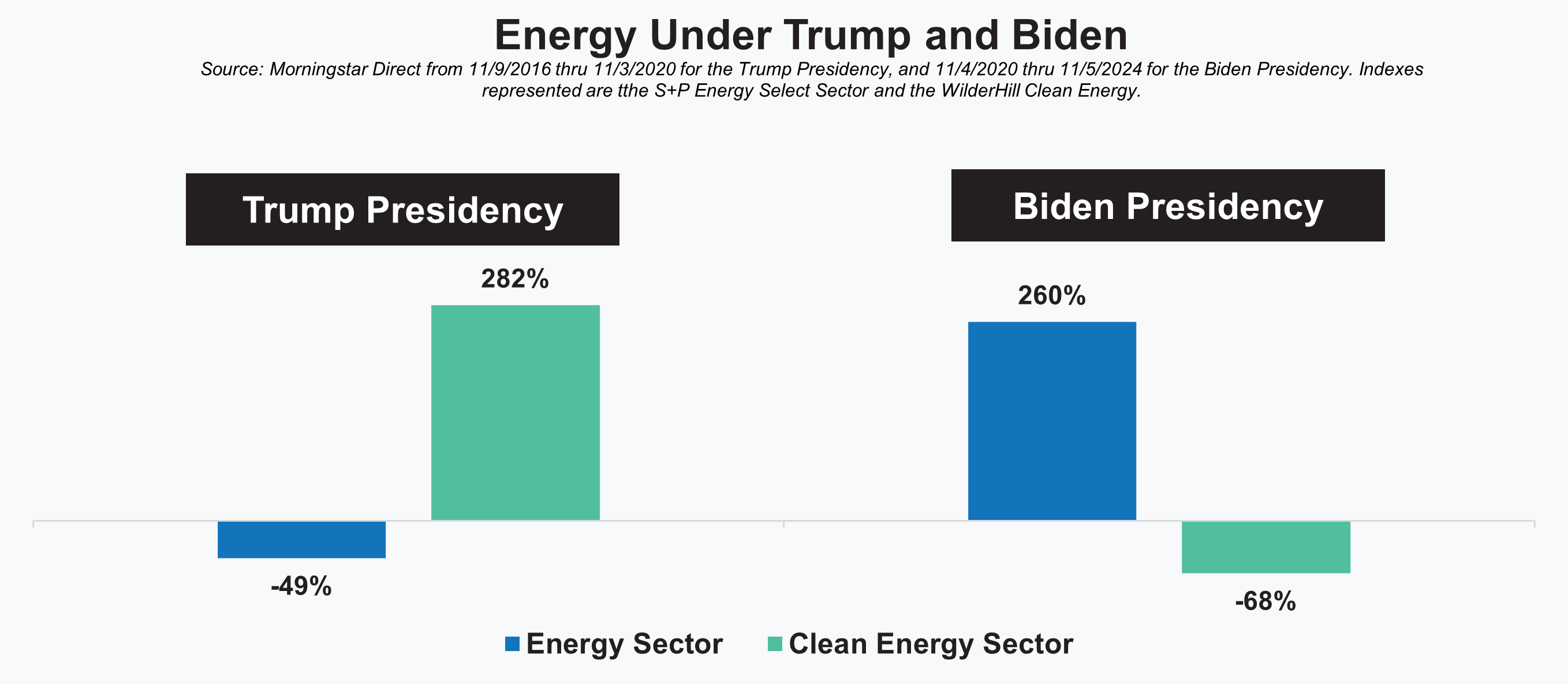

With credit to J.P. Morgan for pointing this specific example out, let’s look at the returns for traditional energy and clean energy over the past 8 years/2 administrations. President-elect Trump is very pro-traditional, fossil fuel energy and critical of efforts to develop renewable energy. It’s a strongly held view that he’s conveyed over each of the past three presidential election campaigns. President Biden, on the other hand, campaigned on scaling back traditional energy efforts and providing government support to renewable energy efforts.

Given those starkly different initiatives under each of the past two administrations, the returns of each provide an interesting, if not extreme, example of how policy isn’t the driving market force that many may expect. In this case, as our graph shows, traditional energy did quite poorly during the first Trump administration while clean energy surged. That narrative then completely flipped during the Biden administration.

Again, policy may matter, but we urge investors not to put too much faith or emphasis on what that may mean for specific markets or markets as a whole. Other factors, such as valuations, often matter more and is why we prefer to keep our focus squarely on them.

As always, if you have any questions, please email me here.

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Want to get insights right to your inbox?

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

November 12, 2024

November 12, 2024

Back to Insights

Back to Insights