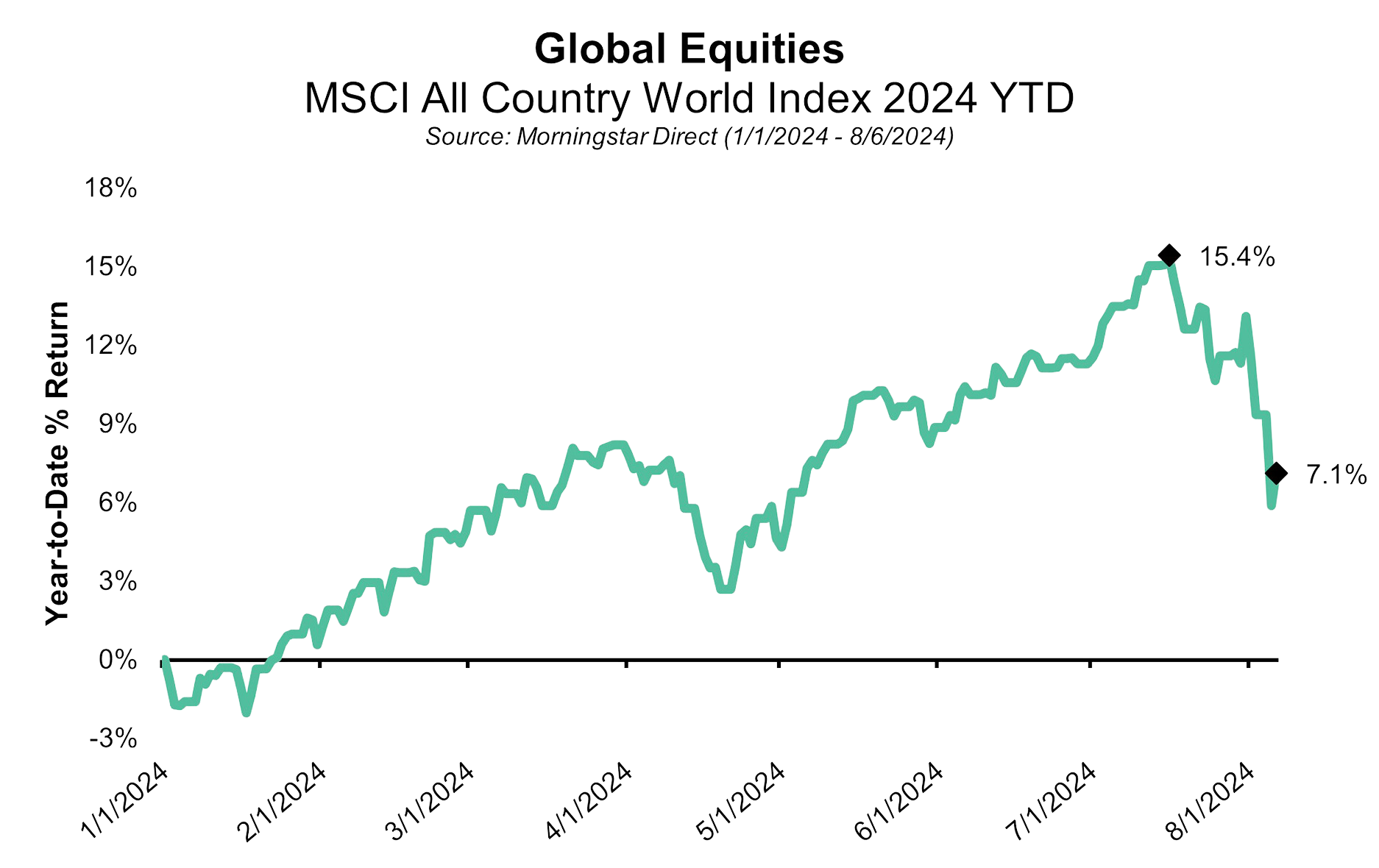

The market recovery on August 6 may have allayed some investors’ worst fears, but global equity markets remain well off their highs – levels set only a few weeks prior. In fact, year-to-date returns have now been cut roughly in half since mid-July (but are still positive!). While markets began experiencing increased volatility and weakness in July, it wasn’t until the calendar flipped to August that the negative momentum really picked up.

So, what changed? What caused the market to drop nearly 9.9% over the course of just three weeks and immediately after hitting a new all-time high on July 16? We’ll get into some of the data and details, but the short answer (in my humble opinion) is complacency. Over the course of the last year, we’ve watched Wall Street and investors in general shift from economic soft-landing skeptics, to optimists, and finally to believers. Never mind that the Fed doesn’t have the best (or any?) track record in engineering economic soft-landings, investors seem to have convinced themselves that this was going to be the time that they finally “landed the plane.”

Investors and equity markets had begun to price in not just the possibility of a soft-landing for the economy, but that it was more likely than not. When it comes to the financial markets, over-confidence around a specific outcome is generally high risk, low reward – not a good tradeoff. If that view proves correct, the market has already priced it in, and upside is limited. If that view proves incorrect, however, we get a reaction like we’ve seen since the end of July. To be clear, a soft-landing is still a possibility, but the market is no longer treating it as if it’s the most likely outcome.

Now for the Data + Details!

Despite some wavering economic momentum the last few weeks, it was a disappointing jobs number last Friday, August 2, that appeared to finally shift the narrative around a soft-landing from “probably” to “not so fast.” While this caused the aforementioned selloff in stocks, meaningful adjustments also affected bonds and expectations for the Fed.

As of this writing, the 10-Year U.S. Treasury is now back below 4% and has seen its yield fall by nearly half a percent in less than two weeks. Not quite the same type of headline material as we saw with the equity market, but still a huge move for bonds. One important additional note about that move, it’s been a positive development for bond investors. Falling yields are a boost to short-term returns and that has helped offset some of the weakness in equity markets for diversified investors.

The change in expectations for what the Fed is going to do has also been significant. We entered 2024 with the market pricing in as many as six rate cuts for the year. Those expectations slowly changed to just one or two cuts through the early part of 2024, but that has now fully reversed. Today, traders are pricing in a 0.5% cut at each of the next two meetings (September and November) and either a 0.25% or 0.5% cut in December. Things have come full circle on the number of rate cuts expected, but unlike last November when those expectations caused a market rally, this time they triggered a selloff.

We’d be remiss if we didn’t at least mention one of the other rumored drivers of some of the recent weakness and volatility. That is what has been referred to in the media as the “carry trade.” Diving too far into what that means, the strategy, or the mechanics is a topic for another, much longer message! What we will say is that given the abrupt change in expectations for the U.S. Fed Funds rate and a newly hawkish bias from the Bank of Japan (BOJ), it is entirely reasonable to assume that this type of strategy (or more the unwind of this particular strategy) has played a role in exacerbating some of the recent market moves.

What Next? What Should Investors Do?

We believe the recent market selloff is first and foremost a good reminder of the inherent uncertainty and volatility that comes with investing. In fact, in nearly all our client review materials we include a chart from one of our asset management partners that does a great job of illustrating that uncertainty and volatility. It shows that since 1980, despite calendar year returns for the S&P 500 Index being positive 33 out of 44 years, the average intra-year drop is greater than 14%. That simply means that at some point in most years, regardless of how the year finishes, equities experience a drop that would be considered a “correction” by market pundits.

The current selloff almost hit 10% this week and may yet hit that 14% level, but it would take a much larger move to really be considered outsized or abnormal, so the first thing we want to convey to investors is not to panic.

The second thing we want to convey, and investors who have worked with us for a while will probably guess this one, is that we want to view such volatility as a potential opportunity. Volatility is inevitable and avoiding it is impossible, so much more productive to try to harness it!

We’ll aim to do that and while we aren’t yet ready to act on anything, we’re watching closely for opportunities. The most obvious would be around our stocks versus bonds positioning. Over the course of the last year, we’ve become increasingly overweight bonds and very recently also lengthened the duration of our bond portfolio. Both shifts that have helped portfolios weather the recent selloff and that may give us an opportunity to capitalize should the weakness in equities (or strength in bonds) persist.

In Closing

The believers in an economic soft landing have had their belief shaken by recent data and that has led those investors to reposition portfolios for a weaker economic outlook than they held just a few short weeks ago. Economic data has been weaker, but interestingly enough a soft landing is still a real possibility. Additionally, though the selloff this week was jarring for many, it was not outsized and not a reason for panic. With our steady, balanced investment approach, we are in a position to potentially take advantage of equities’ weaknesses or bonds’ strengths should the opportunity arise. Stay tuned for updates and as always, call anyone on our team with questions.

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Want to get insights right to your inbox?

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

August 7, 2024

August 7, 2024

Back to Insights

Back to Insights