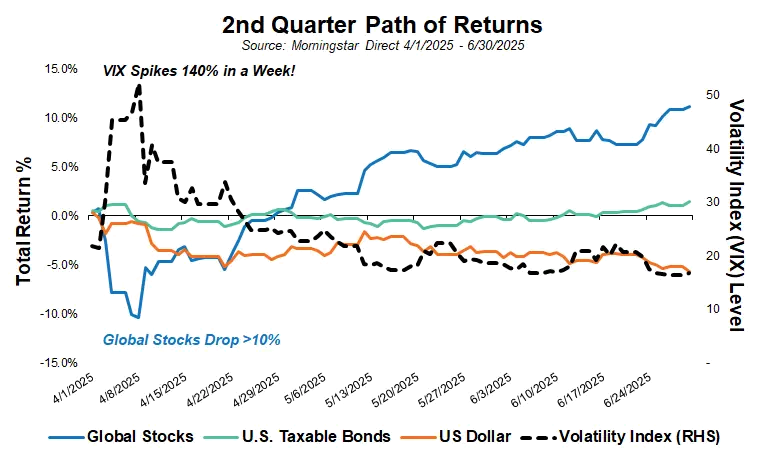

The 1st quarter of 2025 had a fair share of market-moving headlines and volatility, but as the calendar turned to April things kicked into a different gear. After the close of trading on April 2nd, the Trump Administration unveiled their plan for reciprocal tariffs in an event President Trump had referred to as “Liberation Day”. We discussed the early April events in more detail in a video segment this quarter, but the impact to financial markets was swift and for the most part negative.

The reaction by the bond market was relatively muted, but the same couldn’t be said for stocks, the U.S. dollar, and broad market volatility. The administration had communicated their intentions and the timing well ahead of April 2nd, so that was not what caught the market off-guard. Rather, Wall Street had significantly underestimated the initial tariff levels and their global reach.

In the days to follow, global stocks would drop more than 10% and the Volatility Index, sometimes referred to as the VIX or the “Fear Index”, shot up more than 140%. The administration would ultimately put a 90-day pause on most of the proposed tariffs. That pause or suspension would calm market fears and equities would spend the rest of the quarter moving higher. The U.S. dollar, however, did not enjoy the same recovery and continued on a downward trajectory that had actually begun before the April tariff announcements.

Despite early-quarter volatility and the continued dominance of tariffs in the headlines, financial markets enjoyed a positive quarter. Bonds were up only marginally, but stocks surged with global equities advancing 11.5% (and nearly 24% from the April 8th close). Tariff concerns certainly remain, but the 90-day pause, moderating inflation levels, expectations for interest rate cuts, and the likelihood of an extension of the 2017 tax cuts all provided a solid backdrop for the rally.

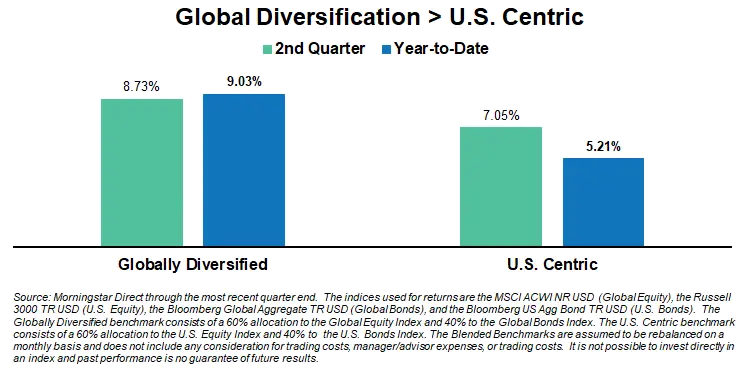

U.S. investors understandably have a home country bias (Fighting the Home Country Bias – Smith and Howard Wealth Management) and pay more attention to what happens in domestic markets. For years, that bias and focus has been rewarded, as U.S. equities have enjoyed a prolonged period of outperformance versus other developed and emerging markets. Whether because of or in spite of the tariffs, that has not been the case through the first half of 2025. International markets, both stocks and bonds, have outperformed the U.S. We know many investors have become more U.S.-centric with their portfolios over time, but the early part of this year has been a good reminder that having a more global, diversified approach isn’t always just about risk – it can also deliver periods of better returns.

Equities

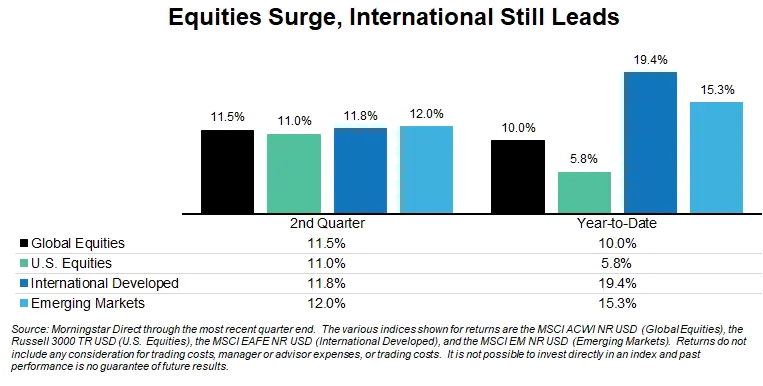

Strength in equities was pronounced and broadly distributed during the 2nd quarter. U.S., International Developed, and Emerging Markets all enjoyed double-digit, positive returns for the period. The year-to-date figures still solidly favor international markets, in no small part due to weakness in the U.S. dollar. Make no mistake, international markets have performed well in local currency terms, but for a U.S. based investor, those returns – when translated back into U.S. dollars – get an additional boost when the U.S. dollar is weaker.

Currency diversification and the potential boost to returns are two of the reasons we’ve advised investors to not get too U.S. centric, especially when it comes to the equity portion of their portfolios.

Last quarter we noted that despite recent outperformance it was too early for investors to start wondering if there had been any type of lasting shift that might favor international markets. It would still be premature to state anything with certainty, but what is becoming apparent is a change in sentiment and capital flows towards international markets. Both are things that can change abruptly, but they are currently trending in a manner that suggests that they could continue to outperform.

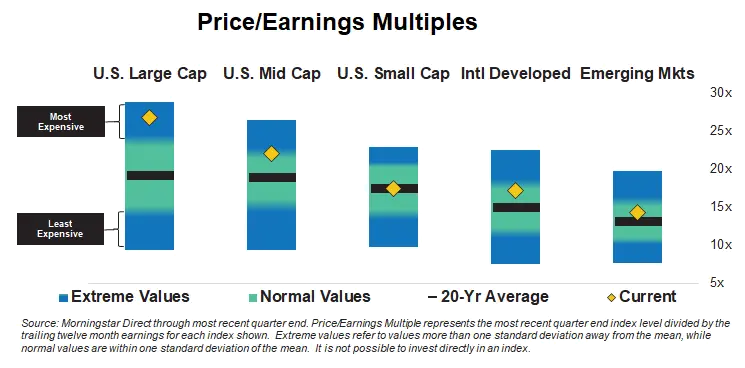

We enjoy periods of positive returns like any other investor, and we are very cognizant of what those returns do to future returns. All else being equal, when returns exceed normal or what is expected, it should lower expectations for future returns. We see that reflected in valuations after the most recent quarter.

While we look at more metrics than Price-to-Earnings multiples, they still do a good job of summarizing our views on equity valuations and where we see opportunities. U.S. Small Cap and Emerging Markets are still at valuations that could be considered average, but they are increasingly outliers. U.S. Mid Cap and International Developed, due to recent performance, is now joining U.S. Large Cap in being closer to expensive than average.

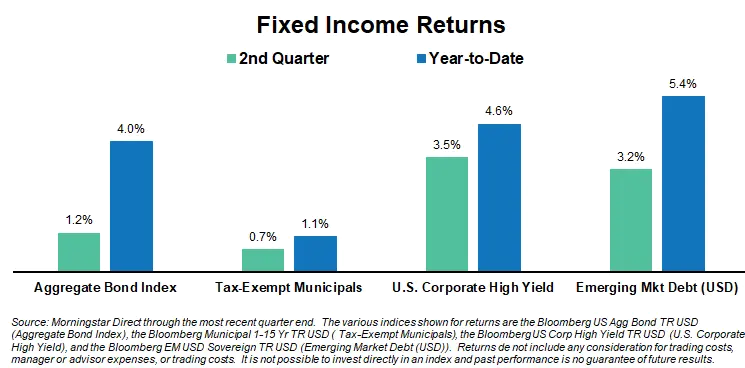

Fixed Income

Returns paled by comparison, but bonds were also positive for the quarter. They weren’t immune to the early April volatility, but experienced even greater volatility around fiscal policy debates. Concerns about the deficit impact of the “Big Beautiful Bill” (or BBB, for short) initially caused a spike in the yield of the 10-Year Treasury, but as time passed that volatility subsided. Notably, despite the yield on the 10-Year reaching a high of 4.60% and a low of just 3.86% during the quarter, the ending yield of 4.24% was nearly identical to the yield at the end of the prior quarter (4.23%).

With overall yield levels mostly unchanged for the quarter, returns in fixed income were more about the “carry” or the income received (rather than changes to bond prices). Corporate High Yield and Emerging Market Debt enjoyed a bit more upside, however, as they benefited from some spread tightening.

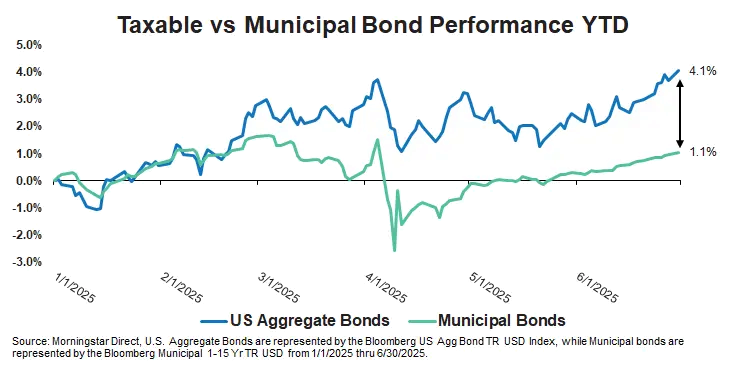

One of the more interesting dynamics, at least for taxable investors, has been the divergence in performance between the taxable and tax-exempt municipal markets. Typically, the two markets move in tandem with returns for tax-exempt municipals being 20-30% lower simply due to the tax benefits that largely offset that discount.

The divergence occurred primarily in March and was driven largely by issues specific to the municipal market. New bond issuance is seasonal for municipalities with the early part of the year typically a high point. That led to an elevated level of supply at a time where one of the tax reform ideas being floated in Washington was the elimination of the federal tax-exempt status of municipal bonds.

The tax-exemption is a long-standing feature of municipal bonds, but the elimination of the feature has occasionally been considered a potential source of revenue during tax debates. The likelihood of this occurring had a very low probability, but it was still enough to give investors pause and create a divergence. Such divergences typically prove temporary, but the gap this year has yet to close.

Taxable or tax-exempt, we still find overall bond yields to be fair. We wouldn’t call them “cheap,” but we believe they are currently a better value on a risk-to-reward basis than equities – although that is more a reflection of increasing valuation levels in equities. One area within fixed income we remain cautious on is lower credit quality strategies, like corporate high yield, where credit spreads remain tight (low).

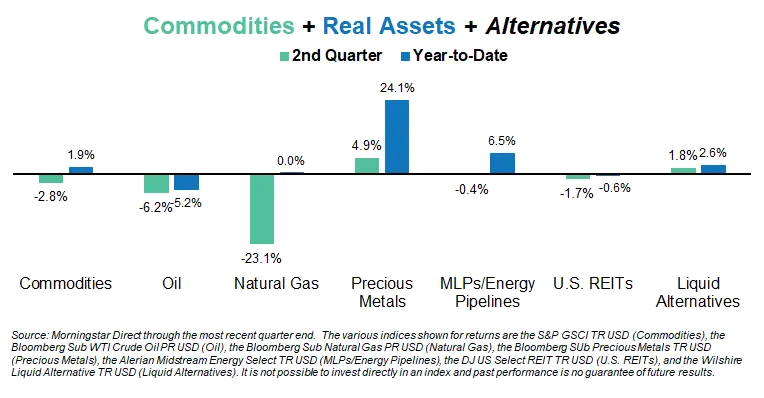

Commodities + Real Assets + Alternatives

Outside of natural gas, it was generally an uneventful quarter across some of the bigger segments of commodities and real assets, as well as an index that tracks liquid alternative strategies. The move in natural gas was certainly significant, but the commodity tends to be highly cyclical and was up 30% in the 1st quarter. The strength in gold was also notable and helped drive Precious Metals to another quarter of solid gains.

For clarification purposes please note that our listing of commodities, real assets, alternatives and returns for the period shown is far from an exhaustive list. We’ve chosen to show broad indices or specific strategies because they tend to be areas of interest for investors and/or areas that we own in client portfolios.

Alternatives, or Alts, tends to be a bit of a “catch-all” phrase for the investment or wealth management industry. Typically, things that fall into the Alts bucket is anything that doesn’t fall neatly into traditional stocks or bonds. While helpful, that leaves undefined a very large variety of investment strategies and vehicles. In this and future quarters, I hope to take a closer look at some of those strategies and detail our views on their merits (or lack thereof). This quarter I took a closer look at Structured equity notes and ETFs in two short video segments.

Thank you for reading. If you have any questions or would simply like to have a conversation around these topics, please call (404-874-6244) or email me ([email protected]).

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Want to get insights right to your inbox?

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

July 11, 2025

July 11, 2025

Back to Insights

Back to Insights