ARTICLE

Economy to Take a Hit Despite Fed’s Intervention

by: Smith and Howard Wealth Management

Note to our readers: This update discusses the implications of the coronavirus on the China, U.S. and global economies and was written March 6, 2020. As of publication (March 9), the world markets have seen a substantial drop, which we know is of concern to many investors. We will issue another update in the next few days specifically addressing the market and our outlook for investors.

The Fed’s emergency interest rate cut on March 3rd of half a percentage point made it clear that officials are taking the economic risks from the coronavirus seriously. But with the number of new cases outside of China rising sharply, it’s unlikely lower interest rates will prevent a decline in activity growth in the coming months.

Manufacturing, the Supply Chain and Consumer Spending

The concerns over supply chain disruption and impact to the manufacturing sector remain, along with growing risks to consumer spending, most notably related to travel and tourism. Falls in equity prices and bond yields in the past few weeks reflect fears that coronavirus cases outside of China will mark the start of a wider outbreak that could deal a blow to the world economy. While the trajectory of the outbreak and any changes to consumer behavior cannot be forecast with any accuracy, the best-case scenario is a moderate decline in global growth over the coming quarters.

The Impact on China

While the decline to world economic growth is difficult to estimate, the damage to China’s economy is more evident. We know for the past month that China’s factories and offices have been closed and most people in China have stayed home.

China’s factories have remained closed for several weeks and are unlikely to quickly become fully functional once reopened. The damage due to lost output may only be partially recouped.

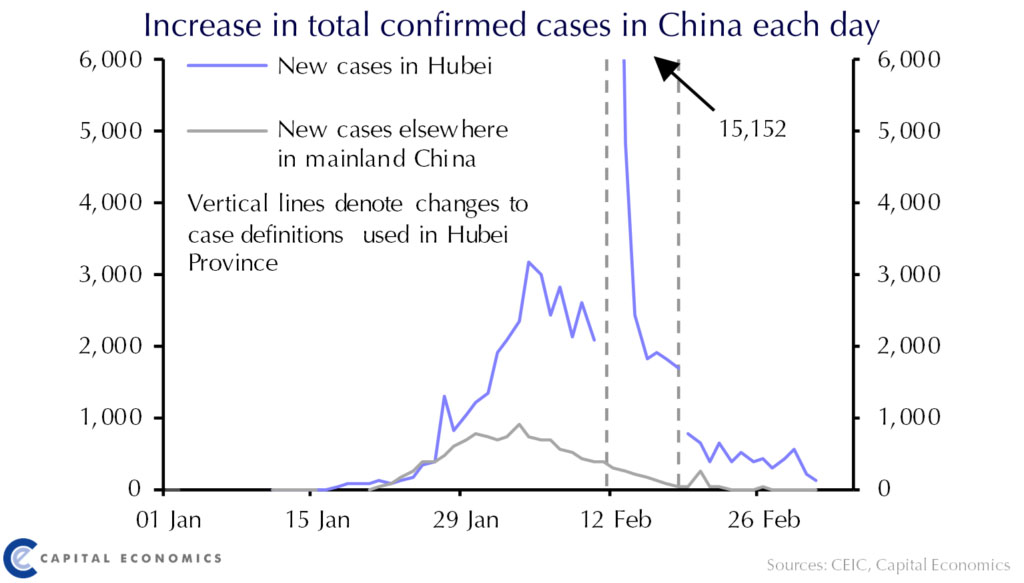

The impact of workers in China staying home will certainly be felt in the coming quarters; however, the positive news is that the number of confirmed new daily cases of the virus in China has dropped close to double digits as noted in Chart 1.

Capital Economics has reduced its forecast for Chinese growth in 2020 from 5% to 3%, which will reduce global GDP growth by 0.4% from 2.9% to 2.5%. China accounts for nearly 20% of global growth.

The containment measures appear to have been effective in reducing the virus spread within China and reports in the coming months will indicate the level to which production gets back on-line as people are able to return to work. Supply chains and the transportation of goods in and out of China will likely remain chaotic for several months as capacity slowly ramps up.

Expansion to Other Countries and Economies

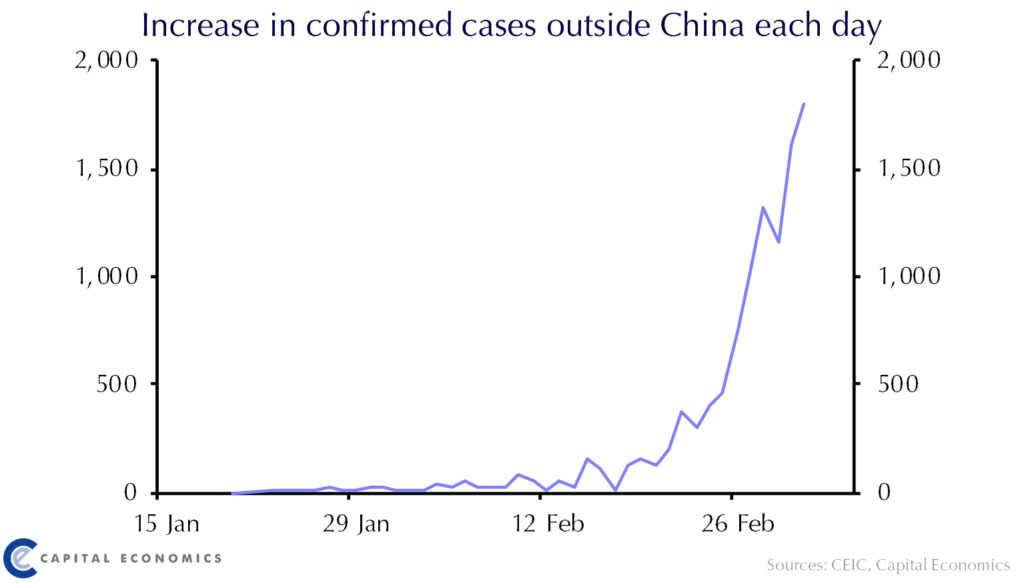

While the virus outbreak in China appears to have stabilized, fears in the week just passed (week of March 2, 2020) have turned to other economies. Chart 2 shows the spike in the number of daily confirmed new cases outside of China since the end of February.

The spread of the coronavirus outside of China, especially the large increase in the number of cases in South Korea, Italy, and Iran, have sparked fears of a global pandemic. News also came last week of the first deaths in the U.S. from the virus. In addition, the number of daily new cases rose sharply to 253 total cases in the U.S. as of March 6th. Assuming the U.S. outbreak follows a similar path to those seen in other countries, the number of cases will continue to rise exponentially over the coming weeks. As testing kits for the virus become more readily available, the numbers of confirmed cases in the U.S. could climb dramatically. Capital Economics projects the number of U.S. cases will peak in the tens of thousands over the next few months and will have a modest impact on global GDP growth.

While it’s difficult to anticipate the ability of the health care providers and government officials in affected regions to contain the virus, if the trajectory of the outbreak follows a similar path as in China, it’s reasonable to expect that containment can be achieved in a few months.

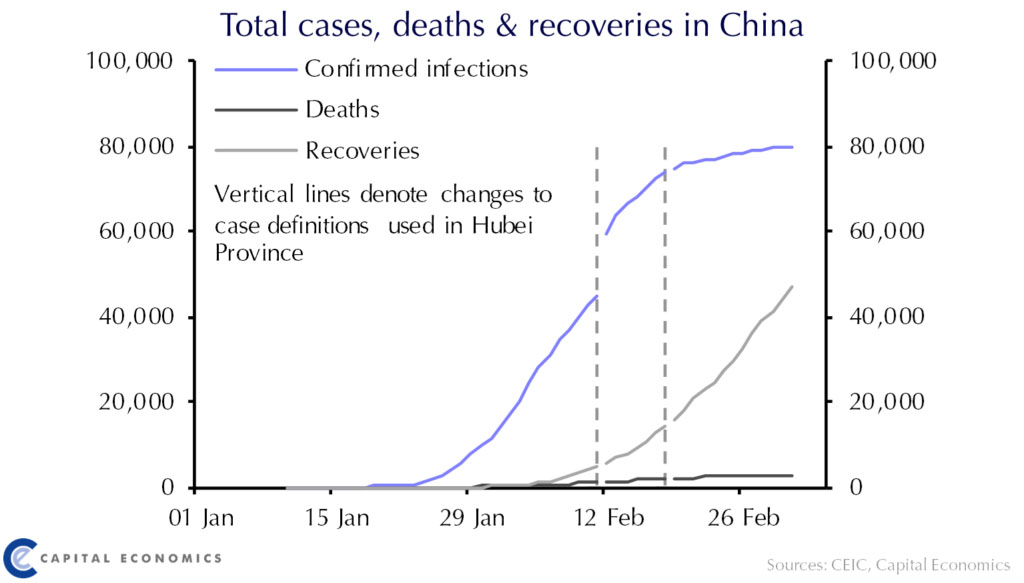

Of course, there are several factors that can impact the actual time frame and the responses of the countries affected may vary widely. As shown in Chart 3, there is encouraging news in that number of total cases in China has plateaued and recoveries have risen sharply in the past month.

Attention is now turning to those countries outside of China showing the largest number of confirmed cases. Per Worldometer, which aggregates statistics from health agencies across the world, the largest number of total cases outside of China as of March 6th are in South Korea (6,593), Iran (4,747), and Italy (4,636). From a global standpoint, South Korea, Italy, Japan, Iran, and Singapore account for 9% of global GDP. Adding that to China’s weight means that almost 30% of the world economy is now significantly directly affected. It is possible that the governments of the newly affected countries will take the same drastic containment measures as China and experience the resulting shutdown in certain business sectors. As more countries are impacted, the existing disruption to supply chains becomes even more complex.

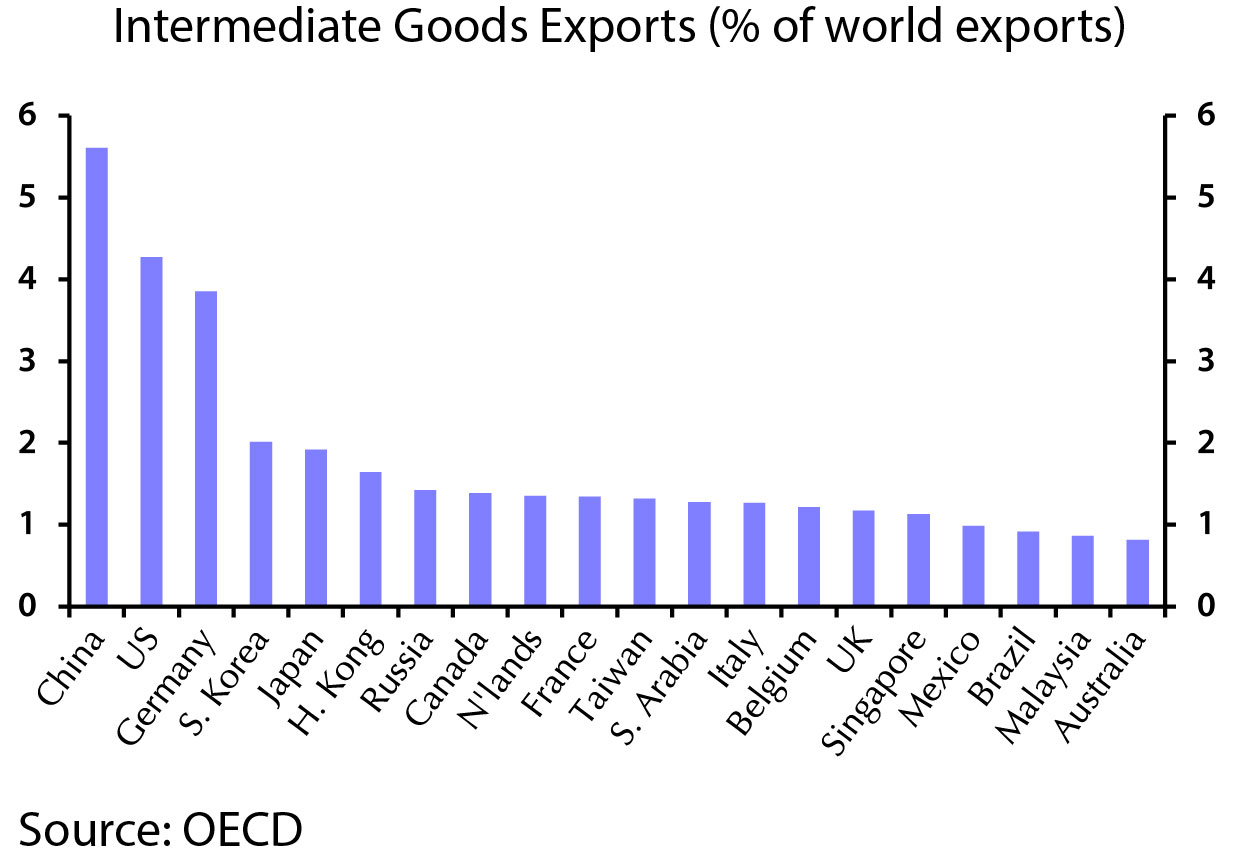

China is the world’s biggest exporter of intermediate goods (items used to create a finished product) as shown in Chart 4 and the most important to global supply chains. Going forward, the U.S. will be key to determining any likely supply chain disruption. While exports do not represent a large percentage of the U.S. overall economy, the sheer size of the economy means that it is an important supplier and purchaser of components from other countries.

Tourism and Travel

In addition to manufacturing, the tourism and travel industry are being impacted with declining revenues as consumer demand is halted. A change in consumer spending in the coming months can have a significant impact on growth and is impossible to estimate at this point.

Will people in other countries start to self-isolate by avoiding public places, shops, restaurants, etc. as evident in China, where passenger traffic and property sales have slumped? Clearly, the further the virus spreads the bigger such effects will be. In the event of a pandemic, the worst affected economies would include those most dependent on tourism, including Mexico, Egypt, and Italy as shown in Chart 5. However, the consumer faces fewer limitations as opposed to a manufacturing firm suffering from down time and lost output. Most pent-up consumer demand can be made up in subsequent months or quarters once the virus has been contained, assuming income has not been impacted.

The Impact at Home

Regardless of the path of the virus outbreak, the U.S. remains the most resilient of the world’s major economies. The U.S. economy had been growing above trend with a solid labor market. The February payroll report of 273,000 new jobs added exceeded forecast of 175,000 jobs and annual earnings growth held at 3%. It’s too early to project any decline in growth in the U.S. economy as the impact has not been reflected in any economic data yet; however, global growth will be impacted due to the expected decline from China in the first half of the year.

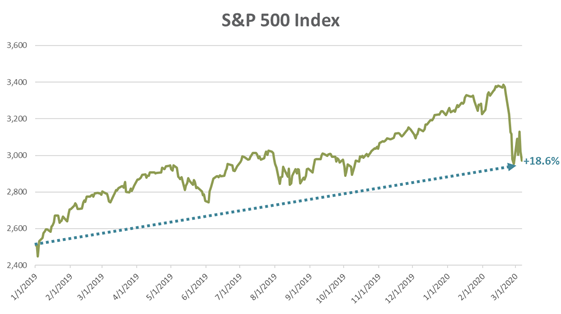

What we do know is that we started the year with an expensive stock market as measured by an elevated price-to-earnings multiple of around 18 and stocks were priced for perfection. After the recent sharp drop, the S&P 500 closed on Friday, March 6th at 2,972 which represents an 18.6% increase from the beginning of 2019. Equity valuations have improved but not to the point where we consider stocks to be attractively priced. Bonds have become significantly more expensive due to investors flocking to the perceived safety of U.S. government treasury bonds and driving yields even lower.

We will continue to monitor these developments and impact to markets in the U.S. and around the world. We appreciate your continued confidence in Smith and Howard Wealth Management and welcome your comments and questions.

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

Back to Insights

Back to Insights