ARTICLE

China and Emerging Markets: Capturing Opportunity While Managing Risk

by: Smith and Howard Wealth Management

April 9, 2019

The growth in China and the Emerging Markets represents a unique investment opportunity. China is the second largest economy in the world and the largest Emerging Markets country by a wide margin. Other EM countries include India, South Korea, Taiwan, Brazil, Russia, Mexico, South Africa, and numerous smaller countries. The massive growth in population in EM countries along with the increase in disposable income is creating a larger “middle-class”, reminiscent of that created by the U.S. “Baby Boomers”.

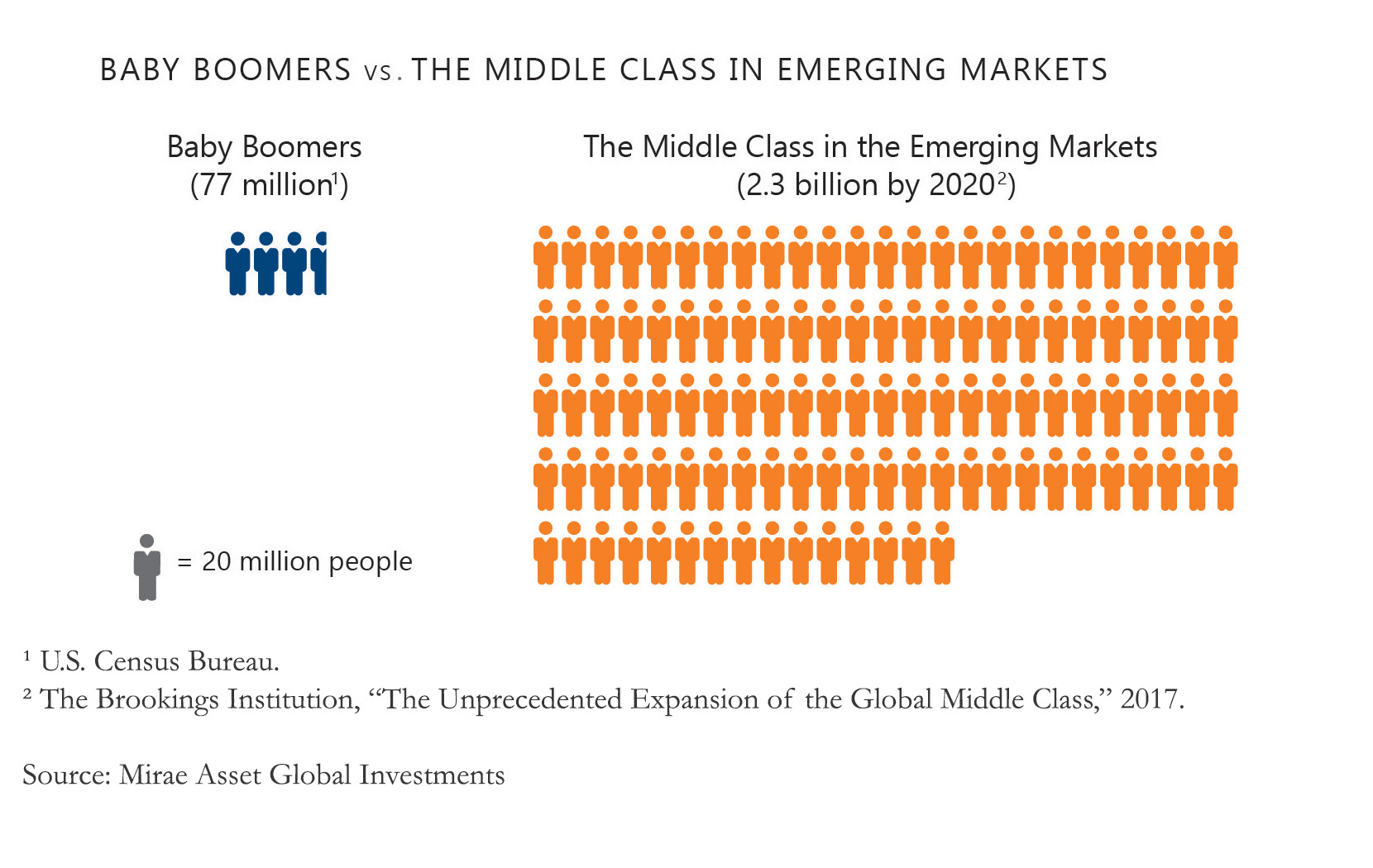

Most Americans know the story of the Baby Boomers born between 1946 and 1964 when birthrates in the United States doubled due to economic and social changes after World War II. This period resulted in 77 million Baby Boomers that contributed to a historical change in economic output and consumption – the expansion of the “middle-class” in the United States brought with it changes in spending and increased consumption activity. Whether it was the purchase of a second car or a home in the suburbs, this consumption-driven economy was born and continues to thrive in the U.S. Now compare 77 million Boomers to the impact of the projected 2.3 billion middle class in the Emerging Markets by 2020 and you can imagine the impact.

Just as with the Baby Boomers, the increase in consumption rate for rapidly growing populations in China and Emerging Markets creates a potential investment opportunity. As with any investment, growth rates alone are not compelling enough but need to be weighed in connection with the current price of the investment. In other words, how much of this projected growth rate has already been priced into Emerging Market stocks? To avoid overpaying for stocks in this fast-growing sector, we have an allocation to a value-focused manager in all but the most conservative strategies.

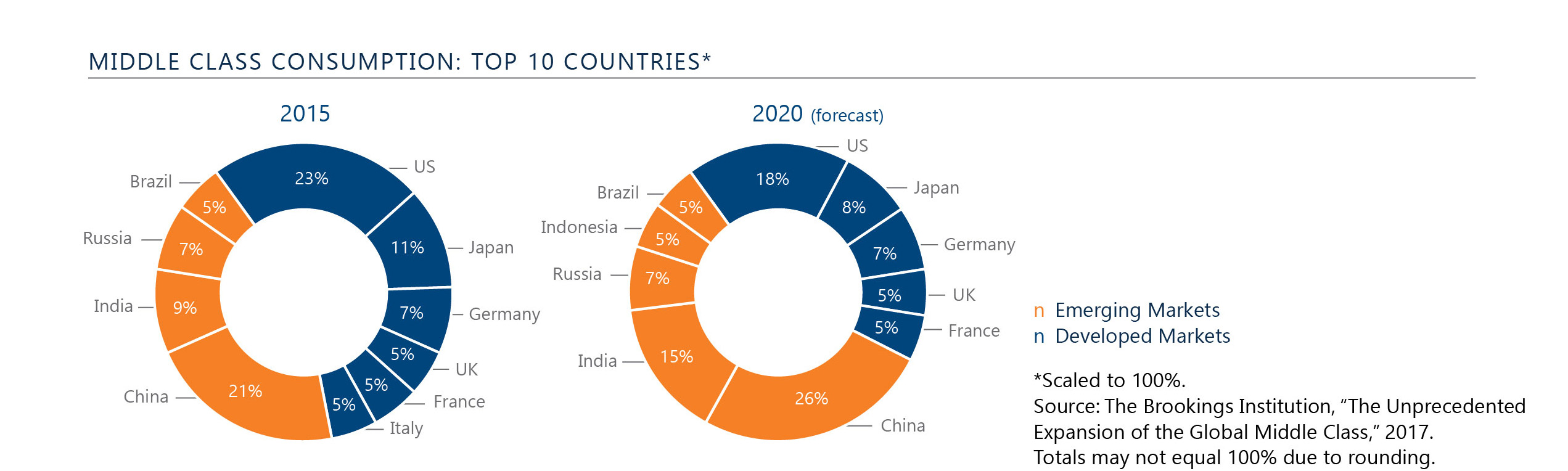

This population surge, along with improving economic conditions has allowed hundreds of millions of people to pursue a higher quality of life, resulting in greater consumption. A vast global competition is underway to provide goods and services ranging from healthcare services, technology, housing, and financial services to these high-growth markets. Refer to Chart 2 which reflects the surge of the Emerging Market Middle Class with the increase in consumption activities and purchasing power. China has the highest projected growth rate and is expected to represent the highest percentage of worldwide consumption by 2020.

From a stock market perspective, China now represents close to 30% of the emerging market index (MSCI Emerging Markets). A large portion of this growth is due to the increasing market share of Chinese technology companies such as Tencent, Alibaba, and Ctrip. These Chinese Internet giants have appreciated considerably in price, aided by China’s relatively young population adopting new technology.

While the potential for high returns exists in this region, it’s also necessary to evaluate the risks, especially considering the high valuations of the Chinese technology sector. One way to reduce the risk is to avoid expensive stocks from a valuation standpoint or price to earnings (P/E ratio). Our solution to gain exposure to Emerging Markets and not overpay for stocks is through the allocation to a value-oriented fund that focuses on stocks with lower valuations.

The value-focused manager we referenced above uses a “bottom-up” approach to select stocks that are trading at a discount to their historical valuation and are also attractive when compared to other companies in the same industry. Most of the expensive Chinese technology stocks that have become a large percentage of the benchmark, do not meet this fund’s disciplined approach to valuation and therefore are not owned in this fund.

For example, the largest holding in the fund is China Mobile which is the largest wireless carrier in China serving over 920 million customers. By comparison, Verizon is the largest U.S. wireless carrier and has 116 million customers per Morningstar reporting. China government-mandated reduction in wireless fees and the elimination of data-roaming charges weighed down earnings for China Mobile in 2018 and the valuation appears attractive at a 12 P/E (price per share to earnings per share). Earnings and revenue are expected to grow as users upgrade to 5G plans over the next few years promising increased speeds and wider coverage areas. A 12 P/E can be compared to the historical average multiple of the U.S. stock market of 17 – 18 P/E and its current multiple of X.

As China’s growth rates decline from single digits to low single digits, the value-focused fund should not be as exposed to potential fluctuations in stock prices from overvalued Chinese companies. One research firm, Capital Economics, expects China’s economy to expand by around 4% to 4.5% over the next year which is below the 6% – 7% rates common in recent years. While there is significant data to support an allocation to Emerging Markets and China from a growth standpoint, the risks should be carefully evaluated. We believe active management in Emerging Markets, with a focus on value stocks, may provide potential for good returns. We will continue to monitor this fast-growing area and welcome any of your questions or comments.

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected. The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results.

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

Back to Insights

Back to Insights