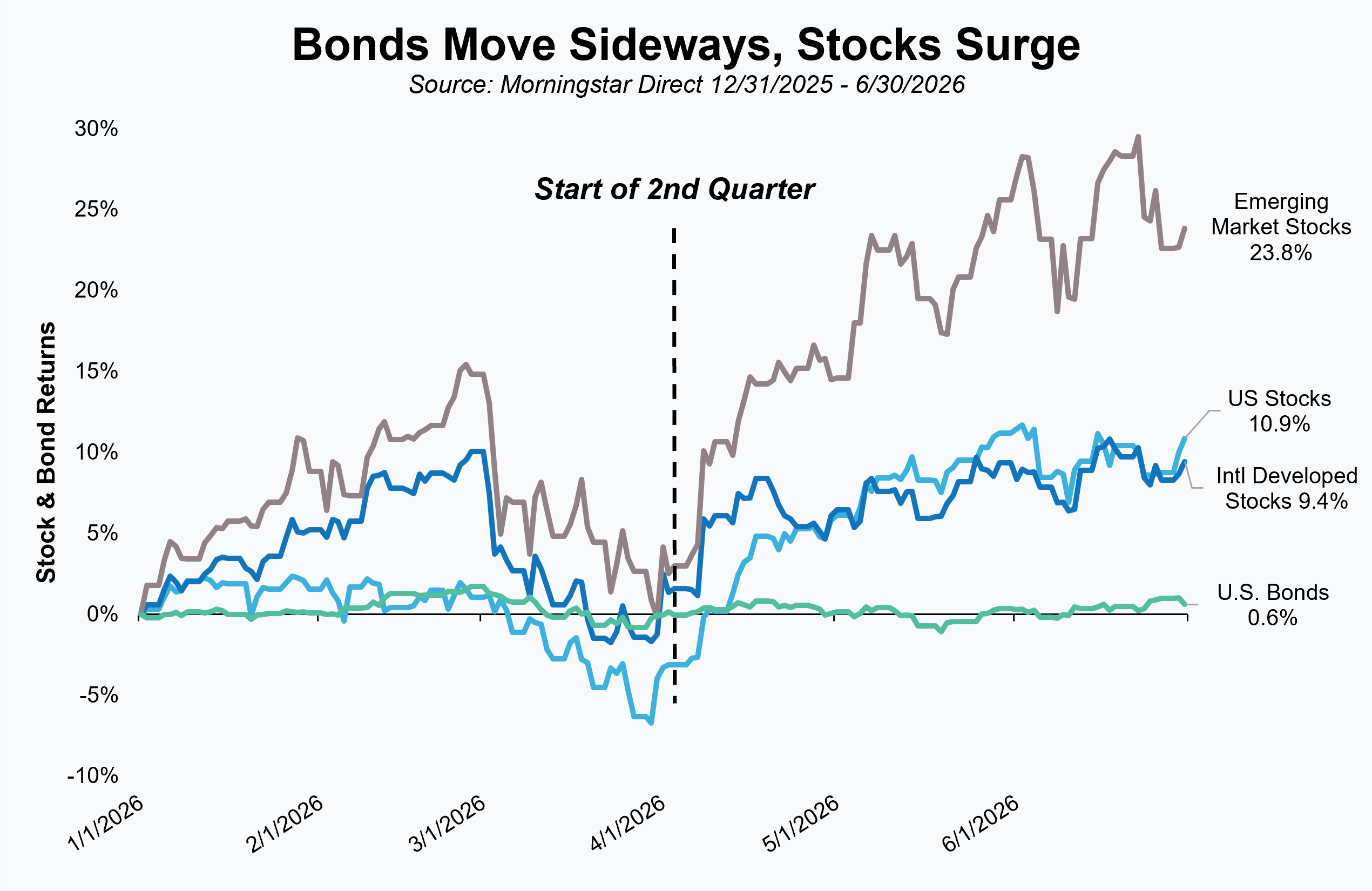

Equity markets delivered a striking rebound in the second quarter. The S&P 500 gained 15.2%, its strongest quarter since 2020. The quarter also served as another reminder that while markets often react swiftly to uncertainty, they have an equally remarkable ability to look beyond it.

Ultimately, the primary driver of stock prices is not the daily news cycle, but the earnings power of the businesses that comprise the market. As fears surrounding the geopolitical backdrop began to subside, investors refocused on what matters most: resilient corporate fundamentals and continued earnings growth.

That shift in focus helped fuel the market’s rebound and reinforced one of our core investment principles. While geopolitical events can create short-term volatility—and often uncomfortable headlines—they rarely determine long-term investment outcomes. Despite concerns about oil prices, inflation, and a prolonged military conflict, corporate earnings growth continued and markets gains followed.

Looking at quarterly returns for the S&P 500 dating back to 1936 (361 observations), the most recent quarterly return of +15.2% ranks among the top 5% and was the strongest quarter since the 2nd quarter of 2020 when the index returned 20.5%.

Equities

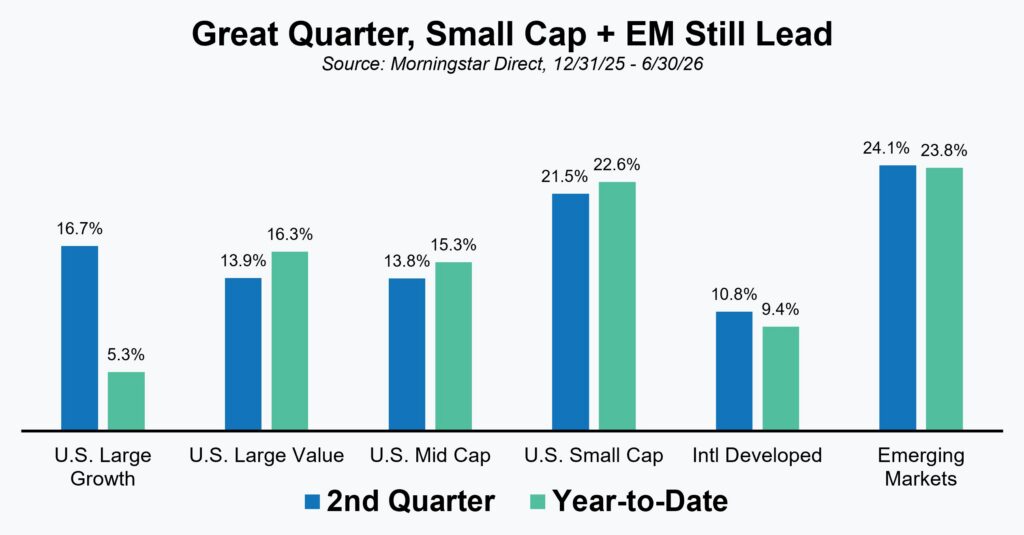

Equity market performance during the second quarter was notable not only for its strength, but also for its breadth. Gains extended across nearly every major asset class and region, with small-cap stocks and emerging markets leading the way. Value stocks have also been strong performers year-to-date.

The strength in emerging markets was particularly noteworthy given the diverse mix of countries and their sensitivity to oil prices. While some emerging market countries did face oil related headwinds, that was more than made up for by strength in Chinese exports, resilient domestic consumption, and AI related capex spending that helped fuel gains in Asian semiconductor and electronic manufacturing stocks.

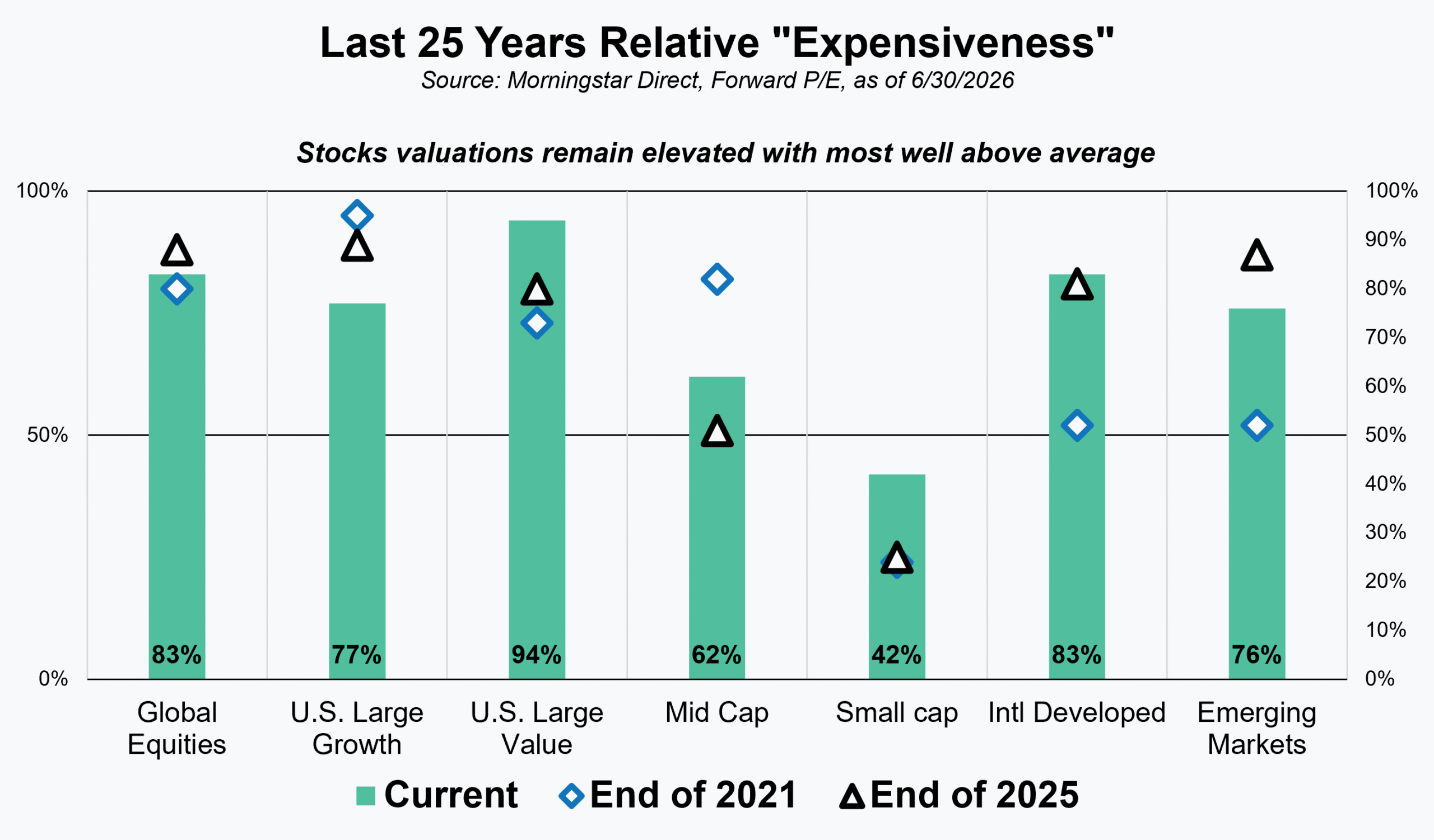

Valuations for most major market segments remains elevated when compared with longer-term measures. Looking at the current forward P/E (Price/Earnings) percentile rank (the mint green bar), most major market segments land in the 80% range. In other words, valuations are more expensive today than they have been over 80% of the time historically. Only mid and small cap stocks score better, but their percentile rank is still only around average (50%). It is hard to argue that equities are cheap by any measure, which means they are already pricing in a healthy degree of optimism and the margin for error has narrowed.

Elevated valuations do not necessarily signal that markets are poised for an imminent decline – periods of above-average valuations can persist for years – but they do suggest that future returns are likely to depend more on earnings growth than on further multiple expansion.

In addition to showing the percentile rank for various market segments, we’ve also included end of year data points for 2021 and 2025. The 2021 data point provides a reference for where valuations were prior to the 2022 selloff and the 2025 data point a more recent reference. While current valuations align fairly closely with those data points for global and U.S. large cap equities, there have been meaningful changes to others. Not surprisingly, strong returns in Small Cap, International Developed and Emerging Markets in recent years have resulted in those markets getting more expensive and further narrowing the opportunity set for valuation-minded investors. As a result, we remain slightly underweight equities in portfolios in favor of fixed income.

Fixed Income

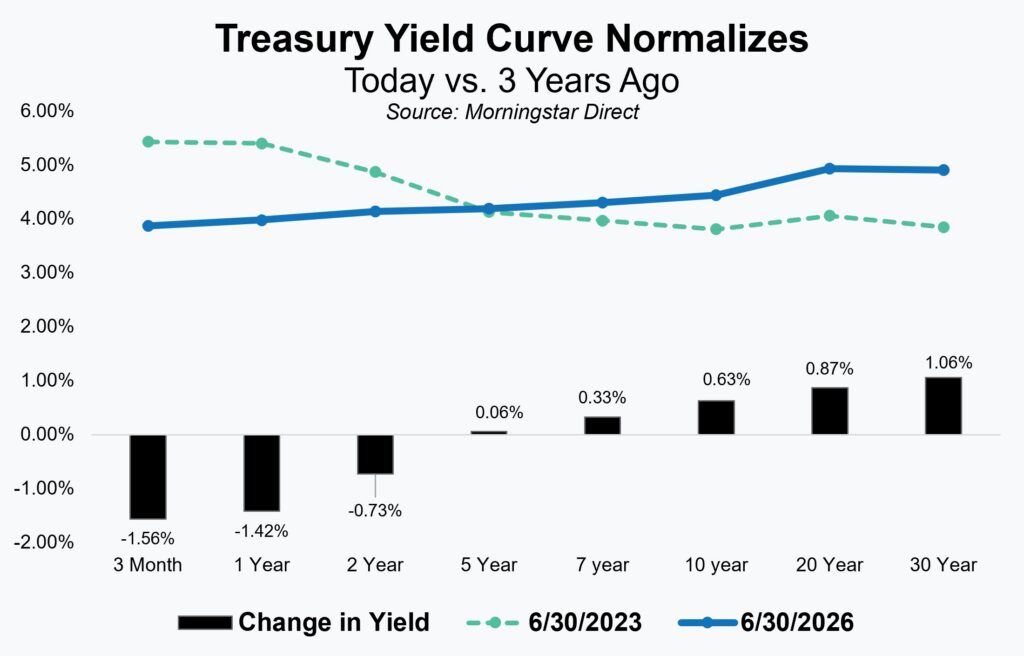

Fixed income returns may have been relatively pedestrian compared to equities, but there were still important developments taking place in fixed income, most notably the continued normalization of the yield curve. When the Federal Reserve last raised interest rates nearly three years ago, short-term rates were above longer-term rates and the yield curve was “inverted”, reflecting a restrictive monetary policy backdrop.

Today, after a cycle of rate cuts and with the Fed now appearing to be on hold (at least temporarily), the curve has returned to a more normal upward slope, with longer-term yields once again above shorter-term yields. This shift marks a meaningful change from the environment investors faced a mere three years ago and the recessionary fears that accompany an inverted curve.

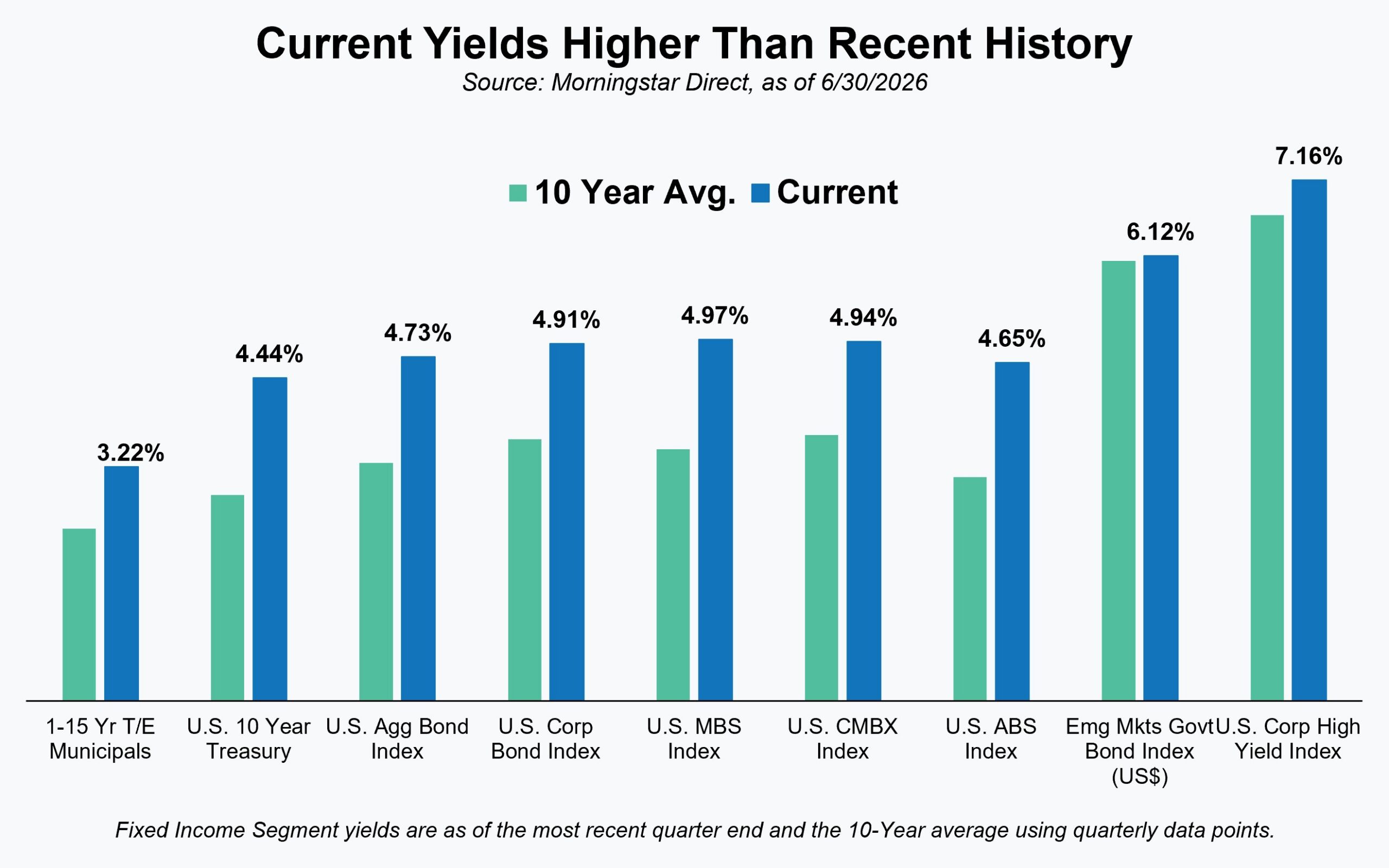

Just as important as the shape of the yield curve is the absolute level of yields available to investors today. For much of the past decade, historically low interest rates left bond investors with limited income and muted return expectations. That environment has also changed dramatically. Even after the Federal Reserve’s recent rate cut cycle, yields across much of the fixed income market remain well above their averages over the last ten years.

Higher starting yields have historically been one of the strongest predictors of future bond returns, meaning today’s market offers a much more compelling backdrop for fixed income investors than they have enjoyed in many years. Bonds are once again positioned to do what investors expect them to do—generate attractive income, provide portfolio stability, all while still contributing to total returns.

More credit sensitive bond segments, like emerging market government debt and corporate high yield, are notable exceptions. Credit spreads remain tight in those markets and although absolute yields are right around their 10-year averages, investors are not enjoying as much additional yield as they are used to when compared to investment grade bonds. With credit spreads tight we remain more conservatively positioned with a greater focus on the investment grade segments of the bond market.

Commodities, Real Assets, and Alternatives

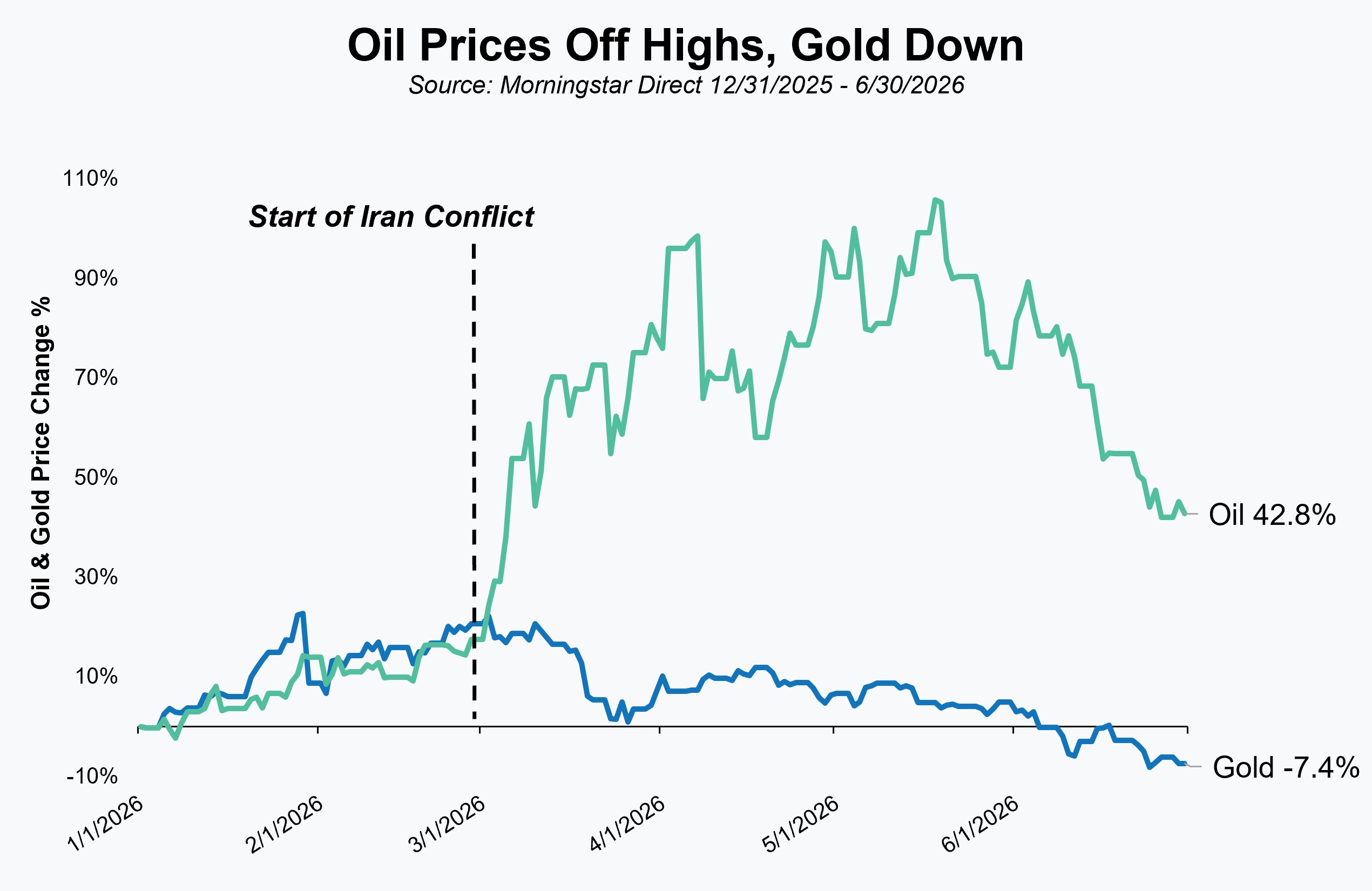

Oil prices remained the focus for financial markets given their impact on inflation expectations and the broader economic outlook. Fortunately, crude prices have retreated from the highs reached a few months ago. They do, however, remain elevated compared to levels seen before the start of the conflict with Iran. Whether they continue to fall will likely depend on whether traffic thru the Strait recovers and how aggressive countries are in restocking their oil reserves.

The spike in oil was to be expected given the nature and location of the conflict, but gold prices followed a more curious path. Typically viewed as a geopolitical safe haven, gold did not provide the kind of protection investors might have expected during the recent period of heightened uncertainty. Instead, after an initially strong start to the year, gold has weakened and is now lower year-to-date. Its behavior is a useful reminder that even traditional “safe haven” assets do not always respond as investors might predict.

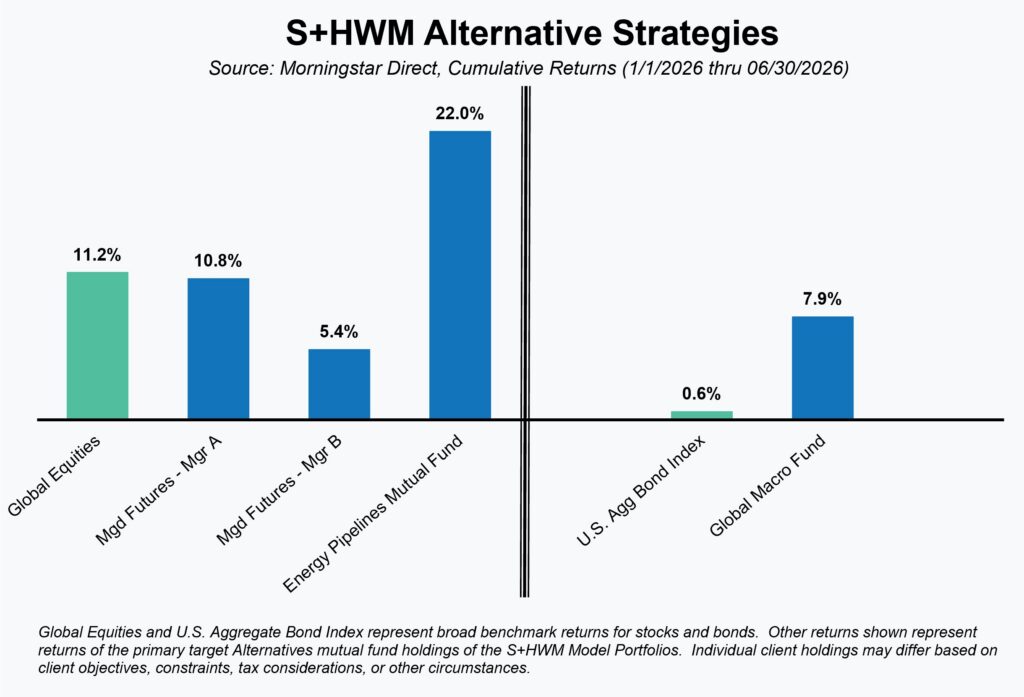

While we expect our preferred alternative strategies to have low correlations to traditional asset classes over time, they too managed to enjoy positive performance this past quarter. The strategies that we use as an alternative to equities, managed futures and energy infrastructure, experienced more modest gains than traditional equities, but they were still positive. Our lone fixed income alternative strategy, a global macro fund, has continued to perform well as geopolitical uncertainty has translated to an increased opportunity set for the manager. On a year-to-date basis, alternatives broadly have been additive and their ability to generate uncorrelated returns has been apparent – particularly during the 1st quarter.

Final Thoughts

The second quarter reinforced a principle we return to often. Over time, it is earnings and valuations, not headlines, that drive returns. Valuations across most equity markets are elevated, which narrows the margin for error and makes future gains more dependent on earnings growth than on further expansion in valuations.

In fixed income, higher starting yields have improved the outlook for bonds, while tight credit spreads keep us focused on higher quality, investment grade segments. Our positioning reflects that balance. We favor quality across both stocks and bonds, we continue to use alternatives to generate returns that do not move in lockstep with traditional markets, and we stay focused on the data rather than the daily news cycle. As the numbers change, so will our positioning.

Unless stated otherwise, any estimates or projections (including performance and risk) given in this presentation are intended to be forward-looking statements. Such estimates are subject to actual known and unknown risks, uncertainties, and other factors that could cause actual results to differ materially from those projected.The securities described within this presentation do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in such securities was or will be profitable. Past performance does not indicate future results

Want to get insights right to your inbox?

Subscribe to our newsletter to get inside access to timely news, trends and insights from Smith and Howard Wealth Management.

July 8, 2026

July 8, 2026

Back to Insights

Back to Insights